Co-author: John Azubuike (@jnazubuike), KEC Ventures.

Note: This article does not necessarily reflect the opinion of KEC Ventures, or of other members of the KEC Ventures team.

Supplying the world with nearly everything is an enormous and complex job: there are things to discuss.

– Rose George (2013-08-13). Ninety Percent of Everything: Inside Shipping, the Invisible Industry That Puts Clothes on Your Back, Gas in Your Car, and Food on Your Plate (p. 142). Henry Holt and Co.. Kindle Edition.

Introduction

Although it is largely hidden from the day-to-day experience of most people, maritime shipping is central to the modern system of international trade and the way our world operates.

According to the International Chamber of Shipping, the international maritime shipping industry transports about 90% of all physical goods traded internationally. To give that some further definition, the World Trade Organization estimates that, in 2014, its members collectively exported merchandise worth $18 trillion.

The U.S. Census Bureau estimates that in 2015 seaborne trade in the United States amounted to $1.56 trillion, with imports accounting for about 67 percent of that total.

Despite its size and importance, the ocean freight shipping industry has remained largely untouched by the kind of transformation that software technology has imposed on other markets. That is beginning to change as a number of startups attempt to build products to serve that market. This post represents our attempt to understand the landscape within which such startups operate.

In the rest of this discussion, we will refer to “startups” as distinct from “companies”. To ensure we are on the same page;

- A startup is a temporary organization built to search for the solution to a problem, and in the process to find a repeatable, scalable and profitable business model that is designed for incredibly fast growth. The defining characteristic of a startup is that of experimentation – in order to have a chance of survival every startup has to be good at performing the experiments that are necessary for the discovery of a successful business model. ((I settled on this definition after reading the work of Steve Blank and Paul Graham.))

- A company is what a startup becomes once it has successfully navigated the discovery phase of its lifecycle. This is the phase during which relatively fixed organizational structures start being built in order to facilitate the firm’s work on behalf of its customers, employees, shareholders, business partners, and society.

KEC Ventures invests in early stage startups. Therefore our primary purpose in studying the ocean freight shipping market is to gain adequate context for the instances when we might assess pre-Series A startups trying to solve problems in this market. We have not yet made an investment in any of the startups in this market.

In the rest of this post we will attempt to;

- Describe the ocean freight shipping market,

- Discuss its market structure,

- Describe the economics of operating within the market,

- Describe and discuss the opportunities that startups are pursuing, and finally we

- Discuss some threats such startups might encounter.

Writing this post is primarily an exercise in learning more about the ocean freight shipping market in order to be better equipped for the conversations we are currently having, and conversations we may have in the future, with startups building products for this market. If we have missed anything please let us know – we lack the expertise and knowledge of industry insiders, but we are willing to invest time in learning. If you are building a seed-stage startup in this market we would love to hear from you. If there are startups in this market we have not heard of yet, we would love to know that too. You can leave a comment in the comments section below, or you can email us directly;

- Brian – brian@kecventures.com, or

- John – johna@kecventures.com.

Lastly, we should point out that how we think about the market may not line up precisely with how industry insiders think about it. However, our purpose is to understand the landscape in sufficient detail to become intelligent investors in startups that have set out to solve problems for this market.

What is Ocean Freight Shipping?

Ocean freight shipping comprises the complex set of activities involved in transporting goods of all kinds from producers in one country to consumers in another country, where the two countries are separated by an ocean or a sea.

We have previously discussed freight trucking, and so in this post, we will focus on the maritime-only portion of the activities that surround ocean freight shipping. In the discussion that follows note that there is a blurring of the lines, somewhat, between the categories . . . Sometimes one category can morph into another, and vice versa . . . For example, a containership might be used to transport a comparatively small amount of bulk cargo.

The market may be segmented as follows;

Container Ships: Most merchandise that is transported by ocean freight travels by container ship. Container ships carry their cargo in reusable, standardized 20- or 40-foot long containers that are designed to be easily transferred from the ship to a truck or train without the need to access the cargo directly. The freight capacity of a cargo ship is described in twenty-foot equivalent units (TEUs).

Liner shipping describes the portion of the maritime shipping market that adheres to fixed schedules on regular routes. According to the World Shipping Council there are 500 liner shipping services currently in operation, most in the form of container shipping, accounting for 60% or $4 trillion worth of goods each year. ((See: http://www.worldshipping.org/about-the-industry/global-trade. Accessed Dec. 3, 2016.))

Container ships transport general cargo, or cargo which is poorly suited for bulk cargo shipping operations but which is well suited for containerization. Most general cargo is now transported by containerships.

The chart below shows that there has been relatively steady growth in the worldwide volume of merchandise transported by container ships since 1980. ((This statistic represents the volume of international seaborne trade carried by container ships from 1980 through 2014. Globally, seaborne containerized cargo amounted to around 1.5 billion tons loaded in 2013.))

| Overview of Container Trade | Values | Statistic |

|---|---|---|

Projected container market CAGR between 2015 and 2018 |

4.4% | Details → |

Quantity of loaded freight in international maritime trade |

10047.46 m t | Details → |

International seaborne trade carried by containers |

1,631 m t | Details → |

Container penetration in maritime transport |

66% | Details → |

Estimated value of international seaborne trade |

$15tn | Details → |

| Global Container Fleet | Values | Statistic |

|---|---|---|

Capacity of container ships in seaborne trade |

228 m dwt | Details → |

Global cellular container ship fleet capacity |

15,406,610TEUs | Details → |

Germany’s share of the world container ship fleet |

6.5% | Details → |

| Operators and Ports | Values | Statistic |

|---|---|---|

Number of ships operated by APM-Maersk |

629 | Details → |

AP Møller – Mærsk’s revenue |

$40,308m | Details → |

Port of Shanghai’s container throughput |

36.5m TEUs | Details → |

Bulk Carriers: Bulk carriers transport merchandise that cannot be containerized – mainly raw materials like timber, coal, cement, grain, iron ore, etc. Bulk carriers are equipped with special machinery to aid in the handling of this type of merchandise.

Bulk cargo comes in the form of dry bulk or liquid bulk. Liquid bulk is transported using tankers. Often, bulk cargo is transported in full shiploads.

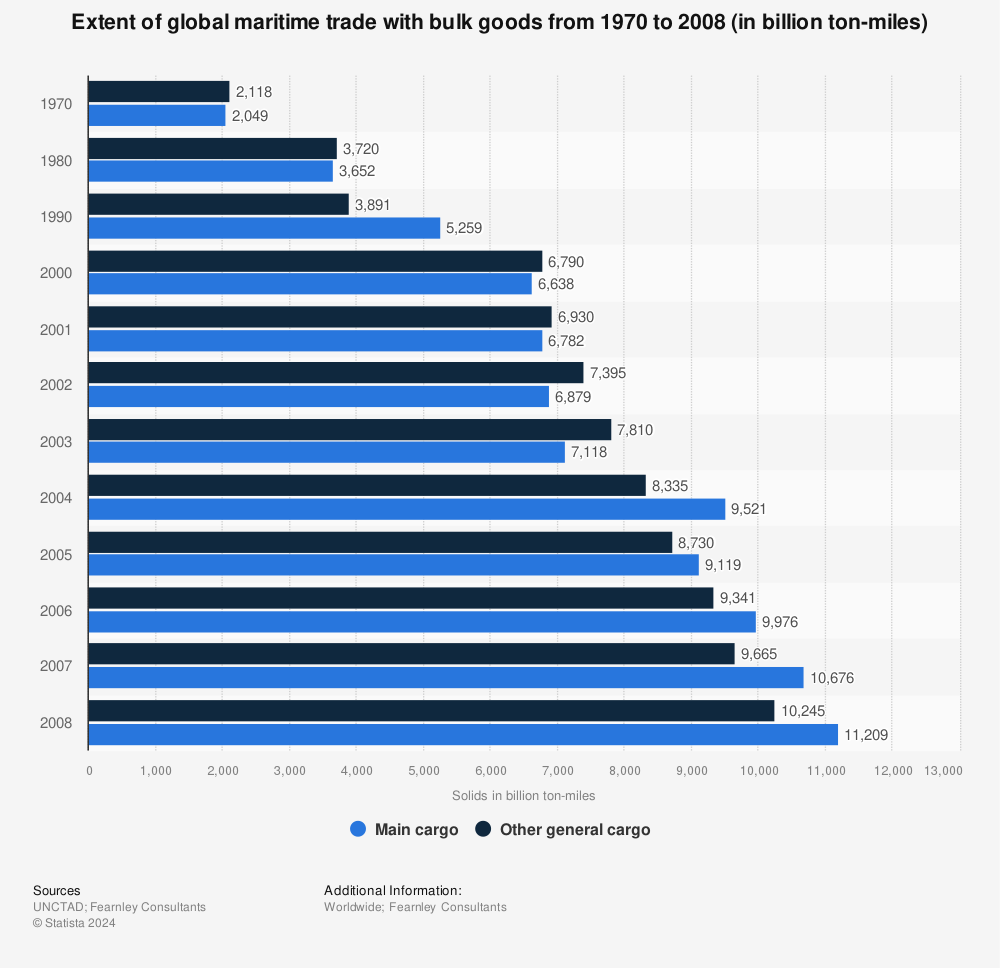

The chart below shows that there has been consistent growth in the worldwide volume of merchandise transported by bulk carriers since 1980. ((The statistic shows the volume of bulk materials shipped by sea from 1970 to 2008 in billion ton-miles. In 2008, 11.2 trillion ton-miles of main cargo were shipped worldwide.”Main cargo” goods include wheat, corn, barley, oats, rye, sorghum, and soybeans.))

Tankers: Tankers are similar to bulk carriers, but are designed specifically for the transportation of crude oil and related products. Tankers are classified according to their deadweight capacity (DWT), with the smallest size group being 10,000 – 19,999 DWT and the largest being 200,000+ DWT. Tankers are also categorized according to the products they carry, crude or product. Based on The Tanker Register 2016 by Clarkson Research, the American Association of Port Authorities estimates that as of January 1, 2016;

- There are 6,085 ships currently in service in the world tanker fleet with an average DWT of 86,211.

- There are another 945 tankers on order with an average DWT of 106,408.

The chart below shows the amount of crude oil that is transported by the world’s tankers.

Specialist Ships: These are ocean-faring vessels designed to function in support of other types of maritime vessels or to perform activities related to specific industries. For example, an ocean-going vessel that’s been equipped to transport entire shiploads of motor cars from Asia to North America would fit this category – ships designed to carry cars are described as roll-on/roll-off (RoRo) ships.

Decades later, when enormous trailer trucks rule the highways and trains hauling nothing but stacks of boxes rumble through the night, it is hard to fathom just how much the container has changed the world.

– Levinson, Marc (2016-04-05). The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger (p. 1). Princeton University Press. Kindle Edition.

Taken together, bulk carriers, tankers, and some specialized ships comprise the tramp shipping segment of the market. The tramp trade describes cargo moved by ships that do not have fixed schedules or make planned port calls. These ships are usually engaged on a contract basis for the transport of commodities, namely crude oils, product (or refined) oils, major dry bulks (those comprising greater than two-thirds of the world dry bulk trade such as iron ore, coal, and grains) and minor dry bulk (those comprising the remainder of the bulk trade such as steel products, forest products, cements, and non-grain agricultural products like sugar).

The three types of charters, or contract under which a shipper can engage a tramp ship, in order of popularity, are;

- voyage charters, under which the ship and its crew is contracted for a particular trip or set of destinations,

- time charters, under which the ship and its crew is contracted for a specified period of time, and

- demise charters, under which the ship is contracted but the shipper is responsible for staffing.

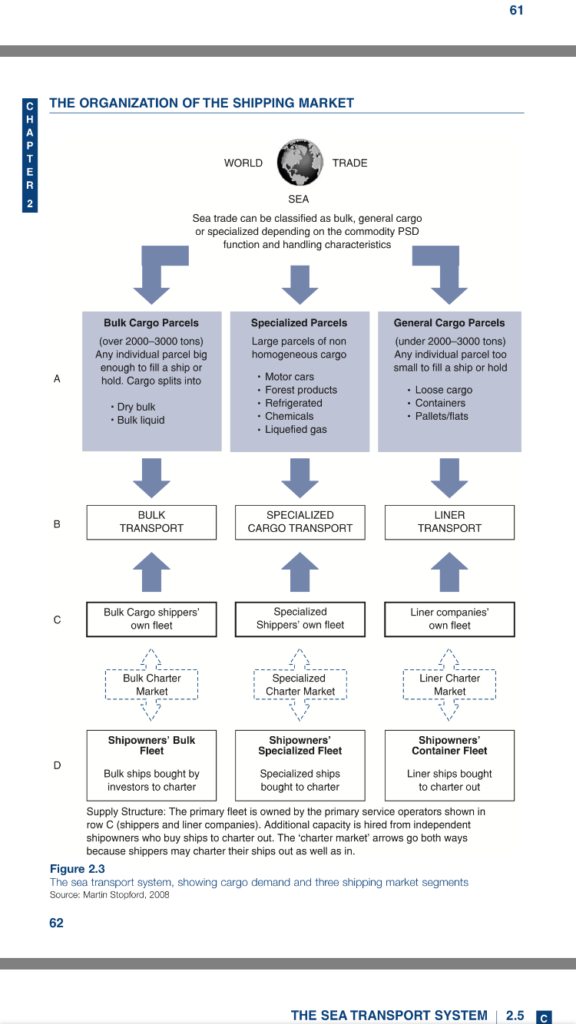

The diagram below is a self explanatory depiction of the organization of the shipping market. It is taken from the 3rd edition of Martin Stopford’s Maritime Economics.

How is The Ocean Freight Shipping Industry Structured?

Shippers: Any entity that pays to have its cargo shipped.

Freight Forwarders: A freight forwarder functions as a consultant to shippers by arranging and taking care of the details related to the import and export of a shipper’s goods. A freight forwarder does not physically ship cargo. Instead, the freight forwarder is a broker who uses extensive industry knowledge, established relationships, knowledge of the law, and experience to get the best deal possible given constraints set by by the shipper. According to the October 2016 update of the industry profile of Freight Forwarding Services published by First Research, the industry generates annual revenues of approximately $260 billion. ((First Research Industry Profile: Freight Forwarding Services, 10.17.2016. Accessed online via New York Public Library SIBL Branch on Jan. 5, 2017.))

Non-Vessel Operating Common Carriers (NVOCCs): An NVOCC is similar to a freight forwarder. However, an NVOCC may go an extra step and physically handle cargo on behalf of shippers in the sense that they will load cargo onto containers that then get shipped by ocean carriers. NVOCC’s generally will accept partial container loads for shipping on the shipper’s behalf. An NVOCC may own or lease its own containers, but does not own any ships.

Ocean Carriers: These are the companies that actually own the ships in which cargo is transported from one place to another. The relationship between the carrier and the shipper is governed by the bill of lading (B/L), a contract that documents the composition of the cargo, the ownership of the cargo, the terms of the agreement to transport the cargo, and eventual delivery from the carrier to the shipper. ((A bill of lading can be non-negotiable or negotiable. Negotiable bills of lading can be used as the basis for various transactions while the goods are in transit.))

The following chart outlines the world’s leading container ship operators.

Other participants in the wider maritime freight market include customs authorities, warehouse operators, freight trucking companies, and various entities that are the end customers of the shippers. For example, Best Buy might be the end-customer for shipments of Apple’s iPhones from Foxconn’s manufacturing facilities in China.

As we have stated previously, liner shipping describes the portion of the maritime shipping market that adheres to fixed schedules on regular routes. Charter shipping occurs on a just-in-time basis, usually brokered through the services of a freight-forwarder or an NVOCC on behalf of the shipper. The term “tramping” is used within the industry to refer to charter service.

Oil companies often own or lease the tankers that they use to transport their goods around the world. For example; BP Shipping was established in 1915, and now operates BP’s international fleet of 49 ships made up of tankers and liquid bulk carriers. ((Source: http://www.bp.com/en/global/bp-shipping/careers.html. Accessed; Jan 23, 2017.))

One anecdote we heard suggests there may be at least as many as a dozen intermediaries involved in the process of getting one shipment of goods from one point to another. However, it is not clear if this is broadly true across the industry or of it applies only to certain segments of the market.

What Are The Economics of The Ocean Freight Shipping Industry?

According to the United Nations Conference on Trade and Development (UNCTAD); ((Report by the UNCTAD Secretariat, Review of Maritime Transport 2013.))

“In general terms, the demand and the supply of maritime transport services interact with each other to determine freight rates. While there are countless factors affecting supply and demand, the exposure of freights rates to market forces is inevitable. Cargo volumes and demand for maritime transport services are usually the first to be hit by political, environmental and economic turmoil. Factors such as a slowdown in international trade, sanctions, natural disasters and weather events, regulatory measures and changes in fuel prices have an impact on the world economy and global demand for seaborne transport. These changes may occur quickly and have an immediate impact on demand for maritime transport services. As to the supply of maritime transport services, there is generally a tendency of overcapacity in the market, given that there are no inherent restrictions on the number of vessels that can be built and that it takes a long time from the moment a vessel order is placed to the time it is delivered, and is ready to be put in service.

Therefore, maritime transport is very cyclical and goes through periods of continuous busts and booms, with operators enjoying healthy earnings or struggling to meet their minimum operating costs.”

In Maritime Economics, Martin Stopford further illustrates the economic and financial challenges that shipping companies must contend with when he says; ((Martin Stopford, Maritime Economics, 3rd Edition, Routledge, 2009.))

“. . . the challenge is to create sufficient financial strength when times are good to avoid unwelcome decisions such as selling ships for scrap when times are bad. It is the company with a weak cashflow and no reserves that gets pushed out during depressions and the company with a strong cashflow that buys the ships cheap and survives to make profits in the next shipping boom. It is not therefore the ship, the administration, or the method of financing that determines success or failure, but the way in which these are blended to combine profitability with a cashflow sufficiently robust to survive the depressions that lie in wait to trap unwary investors.”

In order to develop some insight on which to base our understanding of the economics of ocean freight shipping we have relied on the following sources; ((Please let us know if there are more current references on the topic we did not find.))

- Konstantinos Gkonis and Harilaos Psaraftis – Some Key Variables Affecting Liner Shipping Costs,

- Harilaos Psaraftis, Dimitrios Lyridis, and Christos Kontovas – The Economics of Ships, Chapter 19 in The Blackwell Companion to Maritime Economics, and

- Martin Stopford – Maritime Economics, 3rd Edition, Chapters 6, 7, and 8.

Shipping revenues are affected by the interplay between cargo capacity, productivity, and freight rates. Where revenue increases as each of these factors is maximized by the shipping company.

The costs of operating a shipping fleet are determined by the interaction between operating costs – including periodic maintenance costs; the costs of maintaining the sea-worthiness of the ships in the fleet according to regulatory requirements and the shipping company’s own policies, voyage costs, and cargo handling costs.

Lastly, ship owners have to worry about capital costs which are a function of the mechanism by which the fleet has been financed.

Stopford points out that the shipping industry has not adopted an internationally accepted standard classification of costs, making any discussion about costs in the shipping industry confusing and unnecessarily difficult.

The following variables also play a crucial role in determining the profitability of a shipping fleet operator;

- The mix of different types of ships within the fleet,

- The age of each ship in the fleet – newer ships are typically more profitable to operate than older ships,

- The capacity of each ship in the fleet – bigger ships are generally more profitable to operate than smaller ships as long as the bigger ships do not impose disproportionately higher operating and voyage costs on the fleet operator,

- The fuel efficiency of each ship in the fleet – higher fuel efficiency lowers voyage costs, and related to fuel efficiency is the operating speed of each ship in the fleet,

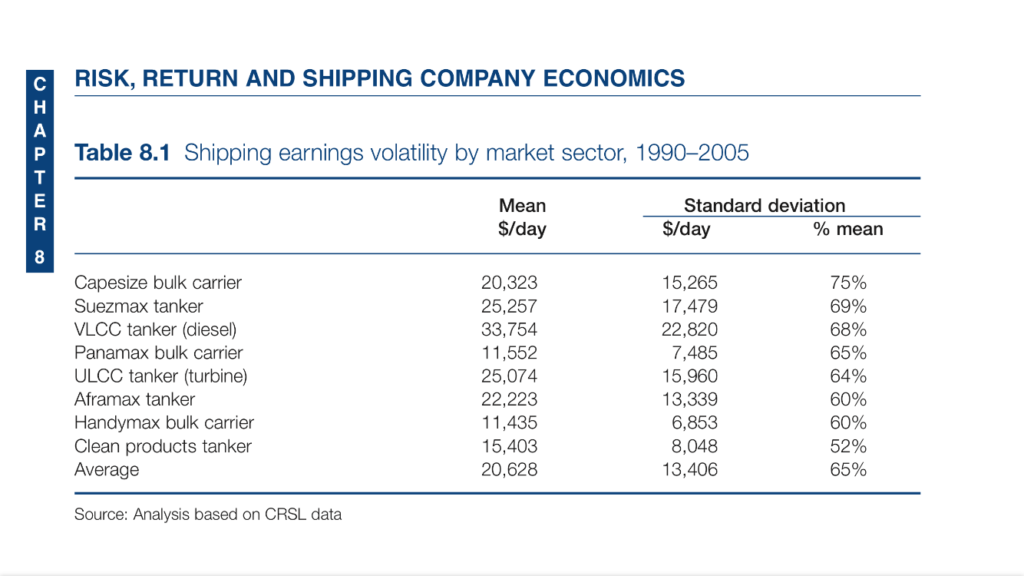

To further ground our understanding of the economic realities of the ocean freight shipping market, the following data and diagrams from Stopford’s book are helpful.

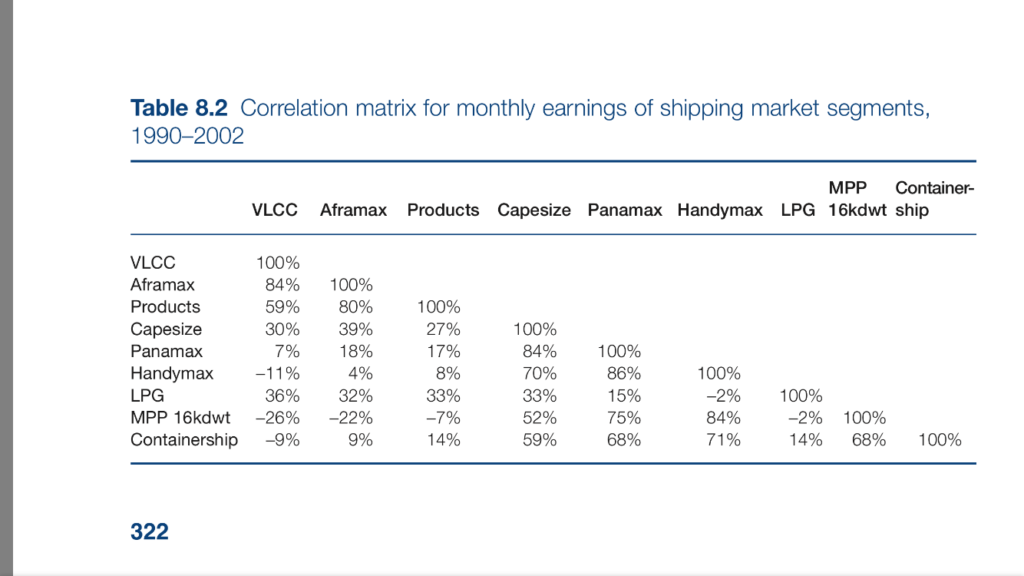

By comparing average earnings per day with the standard deviation of daily earnings, we get a sense of the extreme economic and financial uncertainty that plagues operators of shipping fleets.

In the table below, notice that one way to guard against the revenue volatility that’s evident in the data above is for fleet operators to diversify the types of ships that they buy to compose a fleet. For example, one such fleet might be made up by combining VLCC, Panamax, Handymax, MPP 16kdwt, and Containerships in different proportions that add to 100%. Basically, the fleet operator has to invest in a diversified portfolio of ships in order to protect the fleet from the probability of failure or bankruptcy associated with any one specific ship or class of ships.

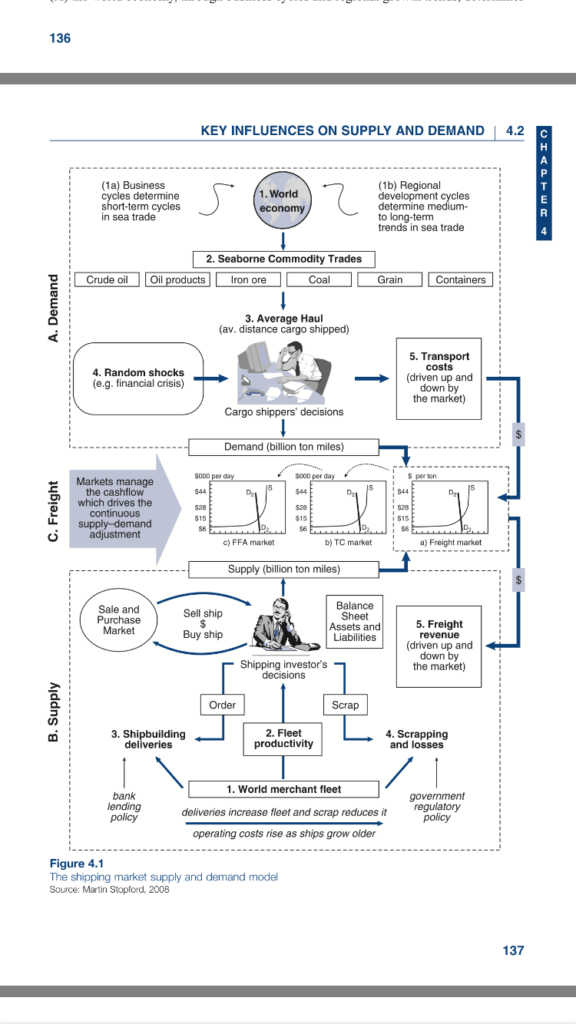

The diagram below outlines the macroeconomic factors that influence supply and demand in the shipping market. Note that there are several factors over which the fleet operator has no control.

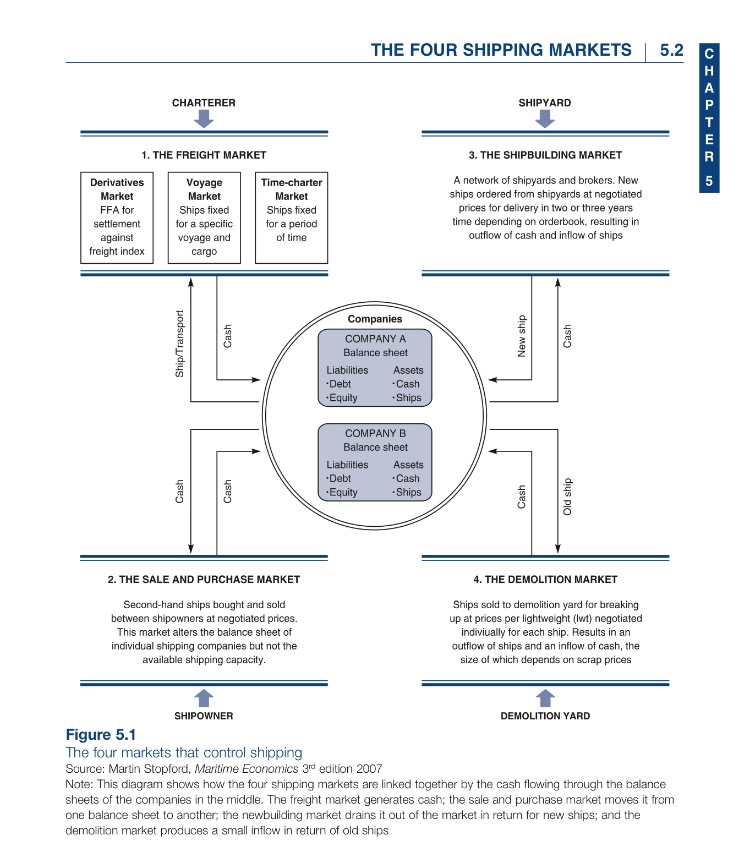

The diagram below outlines the flow of cash and services between the 4 primary segments of the shipping market; The freight market, the shipbuilding market, the sale and purchase market, and the demolition market.

Sabeen Firozali (@sabeenfirozali) is a Vice President at Comerica Bank in New York, where she invests debt capital in technology and life sciences startups. Her experience as a debt investor spans both public and private markets and across many industries, including technology, healthcare, industrials, energy and consumer. She sent us the following comment, which provides additional context to the economics of the ocean freight shipping market;

“I used to cover shippers like Overseas Shipholding Group (OSG) back when I did distressed debt investing. These companies have pretty complex capital structures (For example; each ship is in a different entity). That required a thorough analysis of the assets and future earnings potential from those assets. In 2012 when I was covering this industry, we were really worried about low spot rates for everything from VLCCs to Panamaxes and also a deluge of fleet supply keeping prices low.

This is a double edged sword for startups selling into the market; on one hand shipping companies are highly motivated to find and pay for products that help them operate more efficiently. On the other hand, in the worst case scenario the ships might be scrapped in a desperate bid by some incumbents to avoid bankruptcy. This is not an uncommon occurrence since each ship is an independent entity onto itself, and can be allowed to fail without necessarily putting the holding company at risk.

What Opportunities are Startups Pursuing?

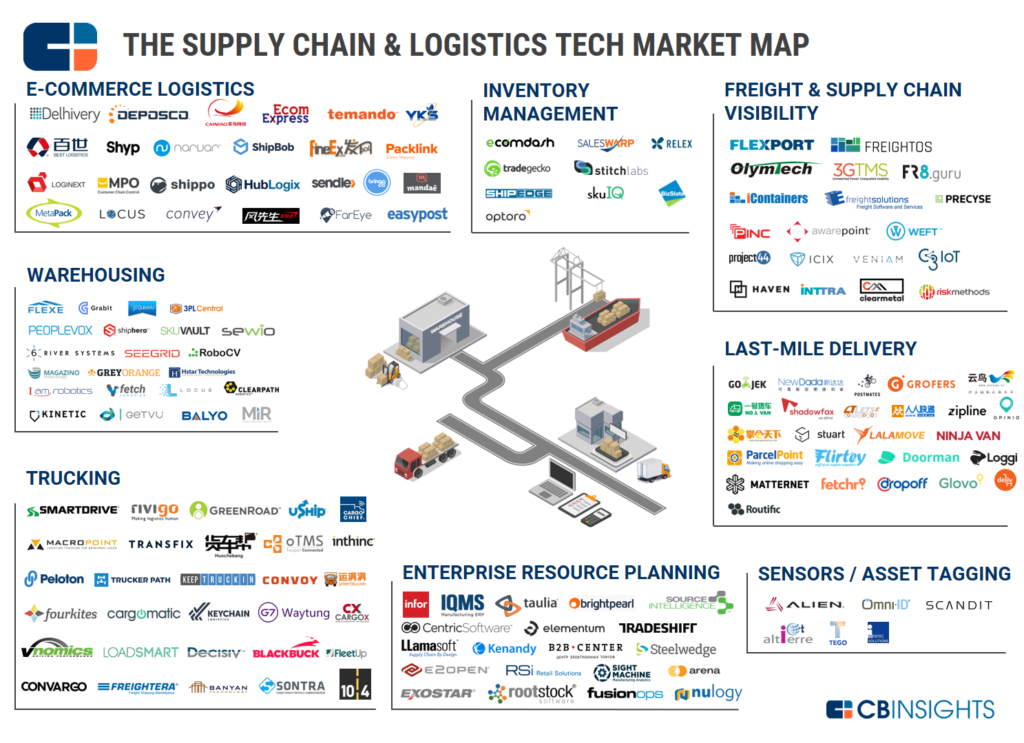

As we alluded to in our post on freight trucking startups, supply chain and logistics is a big market . . . and there are many startups building products to serve that market. This market map by CB Insights lays out the landscape in sufficient detail to provide a sense of the breath of the market for supply chain and logistics software. You can find the accompanying blog post here.

Given how far removed ocean freight shipping is from the day to day experience of most people, it should not be surprising that there is a much smaller number of startups building products for the ocean freight shipping market.

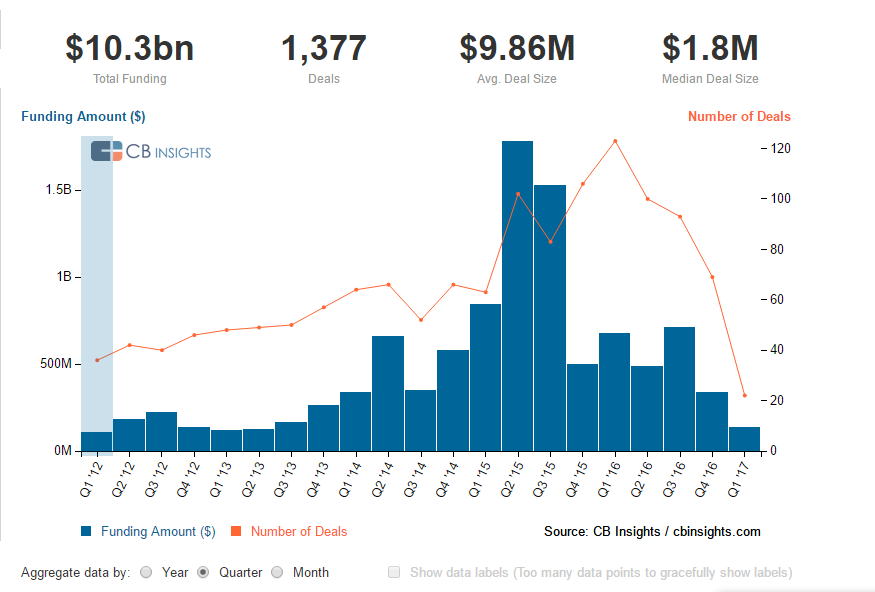

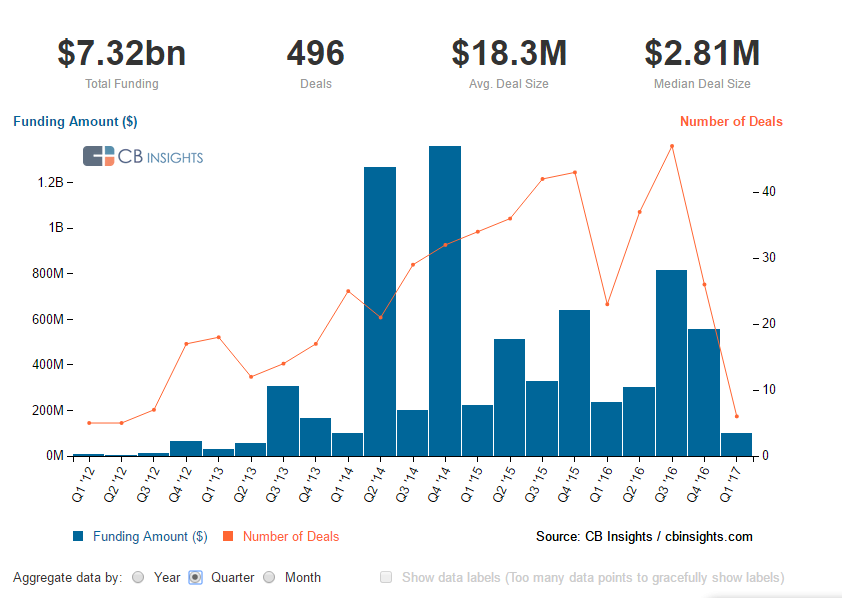

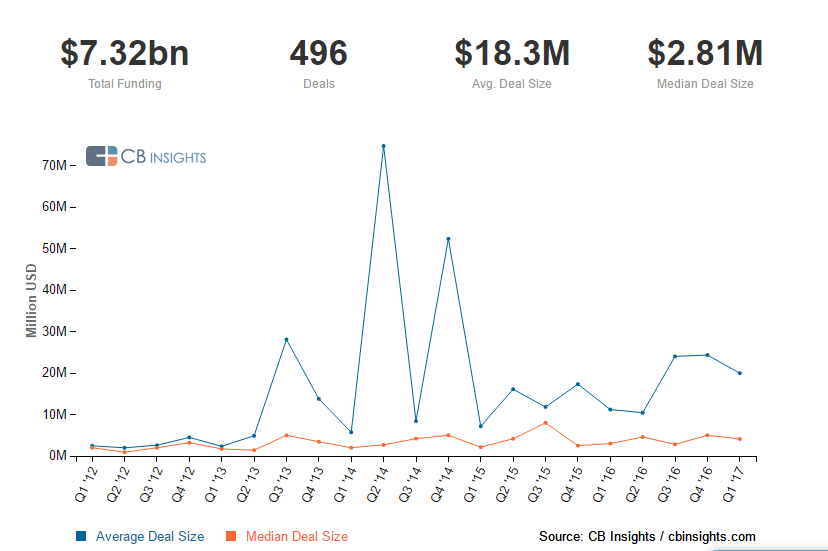

Before we get to the startups, the following data and charts from CB Insights helps to paint of the level of interest among investors. Compiling data specifically focused on maritime startups would have been an incredibly tedious and time consuming process. So, we are using aggregate data as a proxy.

Investments in Startups Building Marketplaces

The next three charts focus on startups pursuing marketplace business models, and reflect investments by institutional venture capitalists and angel investors only. Corporate VCs are excluded, for the most part . . . The database query might have failed to pick up a couple. The data is as of Jan. 30, 2017.

As you can see, funding amounts peaked in 2015 while the number of discrete investments peaked in 2016. One way to interpret this is that, to some extent, the 2016 trend in number of deals may reflect a case of “me-too” investments driven by social-proof bias.

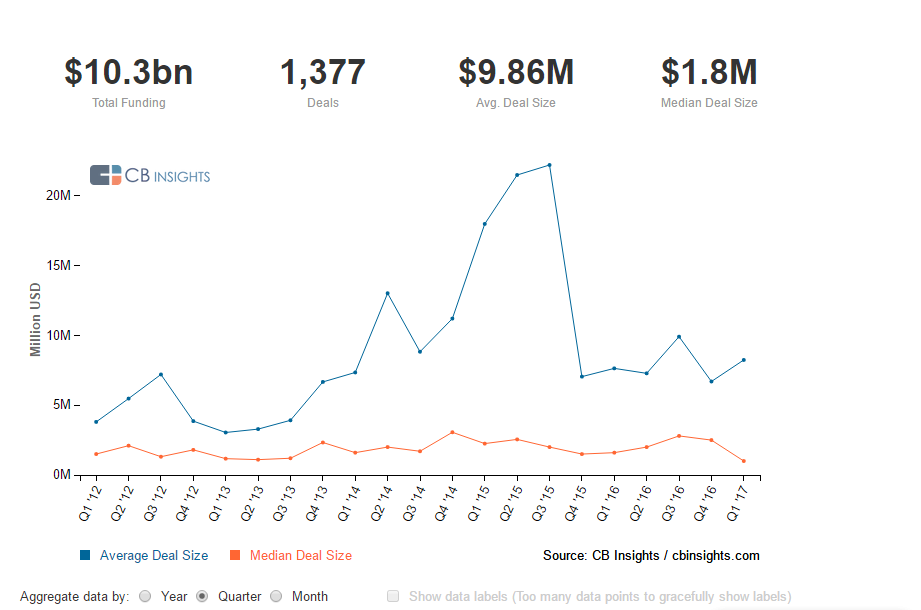

Comparing measures of central tendency in the data, notice that there is dramatic jump in the average deal size in Q2 2015 and Q3 2015, but this trend is not reflected in the median deal size.

The deals below largely account for the spike in aggregate funding amounts, and correspondingly, in average deal sizes for Q2 2015 and Q3 2015, respectively, in the chart above.

- Wish raised $500M from DST Global, Founders Fund, GGV Capital and JD.com

- Zhubajie raised $418.6M from Chongqing New North Zone Goverment Investment Fund and Cybernaut Growth Fund

- Funding Circle raised $150M from Baillie Gifford & Co, BlackRock, DST Global, Sands Capital and Temasek Holdings

- Wallapop raised $100M from Accel Partners, BlackPine Private Equity Partners, Eight Roads Ventures, Insight Venture Partners, NextView Ventures, Northzone Ventures and Vostok New Ventures

- Social Finance raised $1bn from Baseline Ventures, DCM Ventures, Institutional Venture Partners, Renren Lianhe Holdings, RPM Ventures, Softbank Group, Third Point and Wellington Management

- Thumbtack raised $125M from Baillie Gifford, capitalG, Sequoia Capital and Tiger Global Management

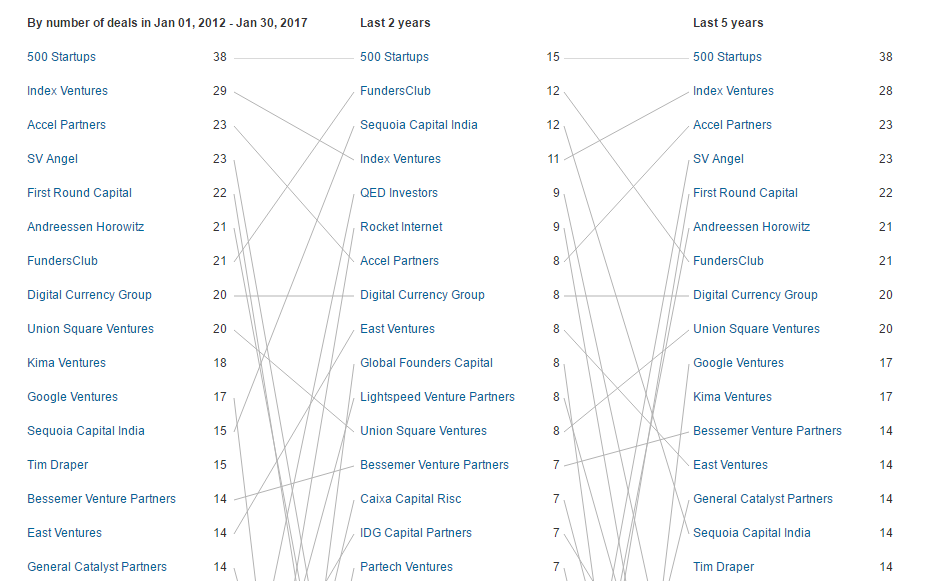

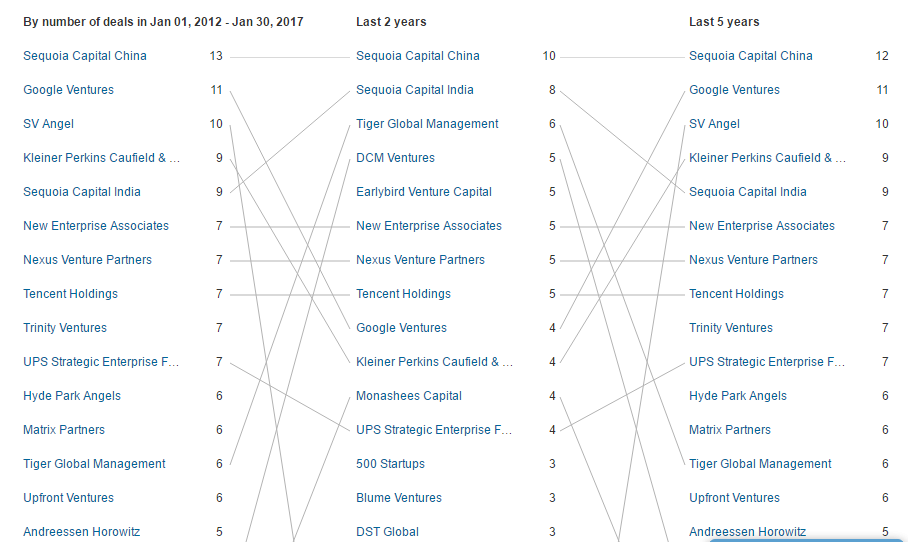

The next chart gives you a sense of the investors who are most actively investing in startups that are building marketplace business models.

Investments in Startups in Supply Chain and Logistics

The next three charts focus on startups pursuing business models in the Supply Chain and Logistics market, and reflect investments by institutional venture capitalists and angel investors only. Corporate VCs are excluded, for the most part – you’ll notice that the query missed a couple. The data is as of Jan. 30, 2017.

Comparing measures of central tendency in the data, notice that there is dramatic jump in the average deal size in Q2 and Q4 of 2014, but this trend is not reflected in the corresponding median deal size in each period.

The deals below largely account for the spike in aggregate funding amounts, and correspondingly, in average deal sizes for Q2 2014 and Q4 2014, respectively, in the charts above.

- New Dada raised $100M from DST Global, Sequoia Capital China & Greenwoods Asset Management

The next chart gives you a sense of the investors who are most actively investing in startups that are building products for the supply chain and logistics market.

Below is a sample of some of the startups building technology products specifically for the ocean freight shipping market. You may recognize some of them in the market map from CB Insights. There is no particular rationale for the order in which we have arranged them here. Descriptive summaries are either copied directly, or based on information, from each startup’s website. Other data presented below is based on information collated by CB Insights, Traxn, Crunchbase, or Mattermark – with CB Insights being the source that appeared to have the most complete information, where it was available at all, and that data is current as of Jan. 25, 2017.

There are undoubtedly tech startups in this market that we have not yet heard about. Let us know about any we have omitted, but which you feel we should be aware of. Full disclosure, we have done some preliminary due diligence on a couple of the startups on this list.

- Summary: An online marketplace for international freight.

- Year Established: 2014

- Location: Portland, OR

- Aggregate Funding: $4,000,000

- Representative Investors: 1517 Fund, GrowthX, Hunt Technology Ventures, NFQ Ventures

- Summary: A real-time price-benchmarking and market intelligence platform for international shipping.

- Year Established: 2012

- Location: Oslo, Norway

- Aggregate Funding: $8,470,000

- Representative Investors: Point Nine Capital, Creandum, Alliance Venture

- Summary: Developed, and markets, foldable shipping containers in order to reduce the cost of empty repositioning.

- Year Established: 2008

- Location: Delft, Holland

- Aggregate Funding: Unavailable

- Representative Investors: CARU Containers

- Summary: Makes it easy to book and track container shipments.

- Year Established: 2014

- Location: London, UK and New York, NY

- Aggregate Funding: $1,300,000

- Representative Investors: EC1 Capital, Northstar Ventures, Partech Ventures

- Summary: A licensed freight forwarder that uses people and software to manage the complexity of international trade.

- Year Established: 2013

- Location: San Francisco, CA

- Aggregate Funding: $91,600,000

- Representative Investors: Y Combinator, Founders Fund, First Round Capital, Bloomberg Beta, Felicis Ventures

- Summary: A web platform with which importers and exporters compare rates in real time and manage their maritime shipments quickly and easily from beginning to end.

- Year Established: 2007

- Location: Barcelona, Spain

- Aggregate Funding: $8,100,000

- Representative Investors: Kibo Ventures, Serena Capital, GrupoRomeu

- Summary: An online marketplace for international freight.

- Year Established: 2011

- Location: Hong Kong

- Aggregate Funding: $27,700,000

- Representative Investors: Aleph, OurCrowd, MSR Capital

- Summary: An online marketplace for international freight.

- Year Established: 2012

- Location: Sydney, Australia

- Aggregate Funding: $590,000

- Representative Investors: Unavailable

- Summary: Connects commodity traders, food producers, and shippers to thousands of logistics providers through one platform.

- Year Established: 2014

- Location: San Francisco, CA

- Aggregate Funding: $13,800,000

- Representative Investors: Data Collective, First Round Capital, Spark Capital

- Summary: A digital ocean freight procurement platform built by freight forwarders, NVOCC’s and logistics service buyers.

- Year Established: 2015

- Location: New York, NY

- Aggregate Funding: $240,000

- Representative Investors: Entrepreneurs Roundtable Accelerator, other undisclosed investors

- Summary: A modern, web-based Terminal Operating System (TOS) built for small to medium container terminals.

- Year Established: Unavailable

- Location: Miami, FL

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: Provides its customers with real-time visibility into the location of ocean freight as well as what’s happening at sea while the freight is in transit.

- Year Established: 2010

- Location: Tel Aviv, Israel

- Aggregate Funding: $15,800,000

- Representative Investors: Horizons Ventures, Aleph.

- Summary: Optimizes global trade logistics through improved route management and increased situational awareness.

- Year Established: Unavailable

- Location: Cambridge, MA

- Aggregate Funding: Unavailable

- Representative Investors: MassChallenge

- Summary: A dynamic online marketplace connecting international shippers with NVOCC’s and Freight Forwarders.

- Year Established: 2014

- Location: Rochester, NY

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: Puts ocean shipping in your hands. Get hassle free shipping rates and schedule your next shipment instantly.

- Year Established: 2014

- Location: Los Angeles, CA

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: Sources and underwrites maritime loans, that are then offered to accredited and institutional investors.

- Year Established: 2015

- Location: Los Angeles, CA

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: A market place for derivative contracts – forward contracts, for the container shipping market.

- Year Established: 2015

- Location: Montclair, NJ

- Aggregate Funding: $510,000

- Representative Investors: Unavailable

- Summary: Nautilus securely collects, reports on, and analyses raw sensor data generated on commercial ships.

- Year Established: 2016

- Location: Brooklyn, NY

- Aggregate Funding: $780,000

- Representative Investors: Root Ventures, Bre Pettis, Marina Hadjipateras

- Summary: A multimodal transport optimization platform applying Industrial Internet of Things and Big Data Analytics to maritime operations.

- Year Established: 2014

- Location: Palo Alto, CA

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: Predictive logistics software for operations in the container-shipping market.

- Year Established: 2014

- Location: San Francisco, CA

- Aggregate Funding: $3,000,000

- Representative Investors: Innovation Endeavors, New Enterprise Associates, Skyview Capital

- Summary: A multimodal transport optimization platform applying Industrial Internet of Things and Big Data Analytics to bring real-time visibility to cargo owners.

- Year Established: Spun-out from CyberPoint in April 2016

- Location: Baltimore, MD

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: Freight management software for freight-forwarding companies. Automates 99% of the freight management process, and automates freight quotes.

- Year Established: 2016

- Location: Warsaw, Poland

- Aggregate Funding: Unavailable

- Representative Investors: Techstars Berlin

- Summary: Blockchain solutions for the shipping market.

- Year Established: 2016

- Location: Melbourne, Australia

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: Software solutions and data products for the oil industry.

- Year Established: 2008

- Location: Vancouver, BC

- Aggregate Funding: $1,000,000

- Representative Investors: Unavailable

- Summary: First platform covering the entire dry-docking process, from first inspection to final report.

- Year Established: 2016

- Location: Oslo, Norway

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: A marketplace for chartering ships and finding cargo based on the user’s location.

- Year Established: 2014

- Location: Scotland

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: Software for the shipping industry.

- Year Established: 2010

- Location:Vancouver, BC

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

- Summary: Paperless trade solutions to automate and accelerate trade operations and finance.

- Year Established: 2005

- Location: Valleta, Malta

- Aggregate Funding: $2,520,000 Debt Financing

- Representative Investors: Unavailable

- Summary: A port or terminal operating system.

- Year Established: 2015

- Location: Unavailable.

- Aggregate Funding: Unavailable

- Representative Investors: PortXL

- Summary: An all in one software solution for reducing fuel consumption for merchant ships.

- Year Established: 2016

- Location: Rotterdam, Netherlands

- Aggregate Funding: Unavailable

- Representative Investors: PortXL

- Summary: Shipamax enables you to internally share fleet openings & the commercial status of each ship. Details can be accessed in real-time by the whole team, across multiple locations.

- Year Established: 2016

- Location: London, England

- Aggregate Funding: Unavailable

- Representative Investors: Dynamo Accelerator & Fund

- Summary: PortXL is an accelerator program focusing on port related industries offering an ecosystem of founders, corporate partners, investors and mentors that support and accelerate the entrepreneurial journey.

- Year Established: 2015

- Location:Rotterdam, Netherlands

- Aggregate Funding: Unavailable

- Representative Investors: Unavailable

While we believe there is a smaller number of startups building products for the ocean freight market, we almost certainly have missed more than we have been able to capture. We are eager to hear about startups we have missed, or to hear about the ideas that people are exploring and hope to launch in the near future.

Everyone loves containers. They see them. They get them. It makes sense. But when you look at number of vessels, container ships are only 10%. They’re inconsequential to bulk, crude, gas/chemical, and cargo. Much more interesting markets to be exploring in my personal opinion.

– Anthony DiMare, co-founder/CEO, Nautilus Labs (via email)

Threats and Opportunities

On a relative basis, if software and automation are “eating the world” as it were, one might argue that the ocean freight shipping market failed to read the memo. However, it ought to be evident from the preceding discussion that there is a small band of entrepreneurs out to change that state of affairs.

While they spare no effort to that end, market analysts at Lloyd’s Register, University of Strathclyde’s Department of Offshore, and QinetiQ have some ideas about what the industry might encounter between now and 2030. The Global Maritime Trends 2030 report is worth reading if this market if any interest to you at all. If that seems too much there’s a more easily digestible summary. ((Accessed; Feb. 5, 2017.))

The report considers three scenarios and how each might be affected by demography, the global economy, demand for resources, and disruptive events. While the rest of the report is very interesting, for the purpose of this study we will highlight the events that the report’s authors believe could be disruptive to the shipping market in general, and hence to the ocean freight market.

- Russia joins NATO, and the balance of geopolitical power shifts quite dramatically.

- The United States Dollar loses its reserve currency status in a disorderly manner, causing upheavals in the global economy.

- There is a major pollution accident in the Artic, causing supply disruptions as well as significant changes to shipping routes.

- Geopolitical changes in the Middle East lead to conflict and constrain energy supplies.

- Unforeseen technological disruptions make formerly popular modes of marine freight shipping obsolete.

- A global economic and geopolitical collapse causes extreme disruptions to trade and commerce.

The technological disruptions that the authors worry most about are;

- Clean coal technologies, which have a significant impact of the amount of petroleum related products transported around the world by ocean tankers.

- Biofuels become sophisticated and efficient enough to have a significant impact on volume of hydrocarbon-based fuels that the world consumes, leading to a steep decrease in the export and import of petroleum related products.

- Deep water exploration for crude oil is curtailed so much that there is a collapse in the tanker market,

- Robotics advances rapidly enough to change the manufacturing patterns for various types of consumer goods in ways that adversely affect international trade via containership since large volumes of consumer goods that were previously imported from China and other markets in Asia are now produced in fully automated factories in the markets that were the biggest importers of such good. The containership market suffers significant losses.

- 3D printing advances to the point where high end products and goods can be manufactured using this method. Together with the large-scale adoption of automation technologies in factories and the use of robots described above, marine trade by containership takes a big hit. Developing markets start a painful transition away from low-paying low-skill manufacturing jobs to high-skill jobs.

- Autonomous ships start to make an appearance in the commercial sector, after being tested for military use and gaining some adoption.

Before we get to 2030, however . . . There are more immediate issues startups and investors operating in this market have to be aware off. Below we highlight some of them.

- Industry turmoil during times of frailty in the global economy can have a disproportionate impact on startups that sell to customers in this market because the customer base is highly sensitive to declines in international trade. Demand for the products and services that startups selling to this market will fluctuate with the business cycle. Industry consolidation is a concern. Also, consolidation within the industry during periods of declining trade may materially shift the balance of power within the industry in ways that could be disadvantageous to startups selling products and services for the shipping market.

- Business practices within the ocean freight shipping market are not as transparent as the practices in other markets that startups often engage with. For example, historically, the industry has maintained the practice of registering ships under a foreign flag – a “flag of convenience”, that differs from the nationality of the ship’s owners. Opponents of this practice argue that it encourages bad behavior within the industry since ships are often registered in jurisdictions with very lax regulations – Panama and Liberia are among the most popular, for example. ((See: List of flags of convenience – Wikipedia.))

- Price negotiations between shippers and carriers are confidential. This can be problematic if a startup’s revenue model is dependent on knowing this information.

- Piracy is an ongoing concern for the industry.

- Employees in the maritime freight industry in the United States are heavily unionized.

- Threats from tech sector incumbents are a real concern.

- Recent articles in MIT Technology Review, Bloomberg, and the Wall Street Journal discuss Amazon’s entry into supply chain management. It has established new sea and air cargo shipping operations, including registering Amazon China with the Federal Maritime Commission. That may be a possible first-step on the path to becoming a full-fledged freight forwarder as is explained in this blog post by Ryan Petersen at Flexport. The threat is such that journalists who follow that market feel that UPS and FedEx may also be under pressure if Amazon succeeds.

- Alibaba has also been making forays into this market. Most recently it has caused a splash with the news that it is partnering with Maersk, the world biggest shipping company, to sell cargo space on containerships operated by Maersk. This article published by Quartz says: “The service reduces dependency on some tasks performed by freight forwarders—middle-men between merchants and shipping lines—and streamlines the export process for merchants. Users can lock in cargo space on certain routes by pre-paying their deposit, Maersk told Reuters. Freight forwarders’ services, such as documentation and customs clearance, can be provided through the OneTouch platform, Maersk said.” The rest of the article is worth reading just to get a sense of the scale of Alibaba’s ambitions for this market. ((This article on the Maersk-Alibaba tie-up provides more context, and some commentary from Maersk executives on how they are thinking about their market; http://www.lloydsloadinglist.com/freight-directory/news/Maersk-Alibaba-tie-up-%E2%80%98no-major-threat-to-forwarders%E2%80%99/68345.htm#.WJog17YrLfA))

We believe that entrepreneurs succeed when they take advantage of a threat or opportunity that others do not notice. Are there any we have missed? If yes, please tell us. ((One opportunity I did not find discussed is the application of industrial internet of things technologies to engine maintenance and monitoring in the ocean freight shipping market. This was somewhat surprising. This article from Deloitte University Press discusses broad IoT opportunities in transport and logistics.))

Automatic Identification System (AIS) – A Key Technology?

The overwhelming majority of maritime carrier vessels have their positions, speeds, and trajectories tracked by Automatic Identification Systems (AIS). AIS systems are usually composed of Very High Frequency (VHF) transmitters and receivers, GPS receivers, maritime electronic links, vessel sensors and display systems. AIS systems are ubiquitous because of Regulation 19 of the International Convention for the Safety of Life at Sea (SOLAS) Treaty. SOLAS was enacted in 1974 by the International Marine Organization (IMO), the United Nations special agency tasked with regulating shipping for its 172 Member and three Associate countries. The purpose of AIS is to provide safety at sea by increasing visibility and capacity to plan around surrounding vessels. The regulation applies to any ship with greater than 300 tonnes of gross tonnage registered in an IMO country.

Traditional applications of AIS include collision avoidance, fleet monitoring, security, search and rescue, and cargo tracing. Should startups begin to experiment with ways to disrupt the maritime freight industry, AIS could prove to be a useful system on which they can build.

Transparency is the first step toward building a highly predictable marine shipping infrastructure. Transparency into a ship’s location allows carriers and brokers to more accurately estimate the arrival of cargo. There is still a ways to go towards that end. In 2013, annual container lines schedule reliability, a measure of the percentage of ships that arrive within their delivery window, fell between 67% and 83%.

Further, the effects of weather and ocean currents complicate the estimability of vessel arrivals. However, we believe that maritime freight would serve to benefit from;

- Systems that would help carriers more accurately assess transit times and eliminate delay days,

- Systems that can use AIS data to draft charter-parties and serve the spot market,

- Technologies that bridge communication between maritime and trucking companies so that both may better serve shippers, and

- Services that lend door-to-door transparency to cargo for shippers.

AIS infrastructure can provide a foundation to future advances in cargo transparency and freight accessibility for shippers.

Wrapping Things Up

Writing this post was primarily an exercise in learning more about the ocean freight shipping market in order to be better equipped for the conversations we are currently having, and conversations we may have in the future, with startups building products for this market. If we have missed anything you feel is important please let us know.

We know how frustrated founders feel when early stage investors (a) do not know anything about a market in which they profess to wanting to make investments in, and (b) make no effort to learn enough about that market in order to have substantive discussions with the founders about what the founders hope to accomplish, and the merits of an investment in the specific startup that founder is building. We do not want to be that investor, we believe in doing our homework.

If you are building a seed stage startup in this market we would love to hear from you. If there are early-stage startups we have not heard about yet, we would love to know that too. If you invest in or have invested in seed-stage startups pursuing any of the opportunities we have described above, or others in the ocean freight shipping market, we’d love to collaborate with you on future investments. If you are a shipping industry insider . . . We’d love to hear from you as well.

You can leave a comment in the comments section below, or you can email us directly;

- Brian – brian@kecventures.com (@brianlaungaoaeh), or

- John – johna@kecventures.com (@jnazubuike).

One last thing. We’d like to express our thanks and appreciation to Britie Sullivan and her teammates at CB Insights for all their help obtaining data that we could not easily gather on our own for this article, and also for the freight trucking article before this. She answers our questions patiently, and often gives us more than we expect. This article is much better because of the data and insights she helped us obtain.

Additional Reading

- Ninety Percent of Everything: Inside Shipping, the Invisible Industry That Puts Clothes on Your Back, Gas in Your Car, and Food on Your Plate.

- The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger

- The Path Between The Seas: The Creation of The Panama Canal, 1870 – 1914

Industry Links

- World Shipping Council: Additional Resources Page

- Federal Maritime Commission

- Institute of Shipping Economics and Logistics

- American Association of Port Authorities

- Lloyd’s Loading List

- World Maritime News

Update: February 8, 2017 at 19:47 to include comments from Sabeen Firozali, and to add footnote about IoT applications to engine Mx.

Update: February 9, 2017 at 05:19 to include Nautilus Labs and MARSEC to list of startups, comment from Anthony DiMare, and link in footnotes to IoT in transportation and logistics article from Deloitte University Press.

Update: February 9, 2017 at 11:16 to include AKUA and ClearMetal, also edit Nautilus Labs’ summary.

Update: February 9, 2017 at 18:51 to correct Sabeen Firozali’s comment. It originally referred to interest rates instead of spot rates. Spot rates were higher in 03-10 and they are directly tied to revenue; higher spot rates lead to higher revenues. When spot rates were high, lots of companies invested in building ships.

Update: February 9, 2017 at 19:31 to correct the aggregate funding amount raised by CoLoadX from $40,000 to $240,000 based on information provided by the co-founders.

Update: June 20, 2017 at 17:22 to fix date typo in updates; change “2016” to “2017”.

[…] Read Azubuike’s guide to business opportunities in the maritime industry here. […]