Note: Although I have not used quotation marks, much of this blog post quotes the people to whom I have ascribed comments almost verbatim. I made slight stylistic and mechanical edits to account for the fact that presented in this format, I do not have the constraints that Twitter imposes on users. Where meaning is unclear or erroneous, I bear full blame for the mistake.

The man who grasps principles can successfully select his own methods. The man who tries methods, ignoring principles, is sure to have trouble.

– Ralph Waldo Emerson

Background: I joined a single family office in December 2008 as the second employee on the team, and as the first employee on what would become the direct investing team. In January 2011 we started building a venture fund from the ground up, KEC Ventures. It grew to $98M of assets under management distributed across a $35M 2011 fund and a $63M 2014 fund, with 51 investments in aggregate. I left KEC Ventures in September 2018. You can read my reflections on my time at KEC Ventures here: #ProofPoints.

I have now teamed up with Lisa Morales-Hellebo to build an early stage fund to invest in startups building innovations to refashion global supply chains. We’re in the early stages of raising the fund, so I am thinking through the issues that every emerging fund manager grapples with. We are simultaneously building The New York Supply Chain Meetup, and The Worldwide Supply Chain Federation – more about that at the end of this article.

This blog post is a qualitative examination of issues pertaining to portfolio construction and portfolio management, from the perspective of a seed-stage manager who is managing a Fund I portfolio that falls somewhere between $10M and $25M of AUM. It is based on a discussion that occured on Twitter in early February 2019.

Before I go much further, some philosophical housekeeping;

- It is my belief that the seed-stage technology venture capitalist’s only goal is to benefit disproportionately from uncertainty. To do this the best seed-stage venture capitalists seek startups that fit an investment thesis, and make investments before other investors would normally invest.

- When I think of uncertainty, I am thinking of a state of affairs in which I have limited information and knowledge, and must make a decision whose outcome I can’t predict because the future is unknown and unknowable. I do not think one can measure uncertainty quantitatively.

- When I think of risk, I am thinking of undesirable future outcomes some of which I can enumerate quantitatively.

A startup is a temporary organization built to search for the solution to a problem, and in the process to find a repeatable, scalable and profitable business model that is designed for incredibly fast growth. The defining characteristic of a startup is that of experimentation – in order to have a chance of survival every startup has to be good at performing the experiments that are necessary for the discovery of a successful business model.

This is the definition I have in mind when I speak of a startup. Early stage venture capitalists will typically invest before search and discovery is complete. This definition is based on a definition by Steve Blank, to which I have added the characteristic of fast growth based on Paul Graham’s observations.

In the remainder of this post, I try to synthesize and organize the comments that arose from my original question on Twitter. I add some commentary of my own where I feel it will be helpful. I am always thinking about this topic so if there is other material you think I should read please send it to me. The easiest way to do so is via Twitter: @brianlaungaoaeh.

I assume that the reader is already familiar with the basics of VC and how a venture fund is structured. If not, here’s a decent introduction from the Harvard Business Review: How Venture Capital Works.

Note: When I make references to modeling portfolio construction for REFASHIOND Ventures’ first fund – which we are in the early days of raising, I am using a spreadsheet model template developed by Taylor Davidson at Foresight. I have known Taylor since 2013 and I couldn’t recommend his work highly enough.

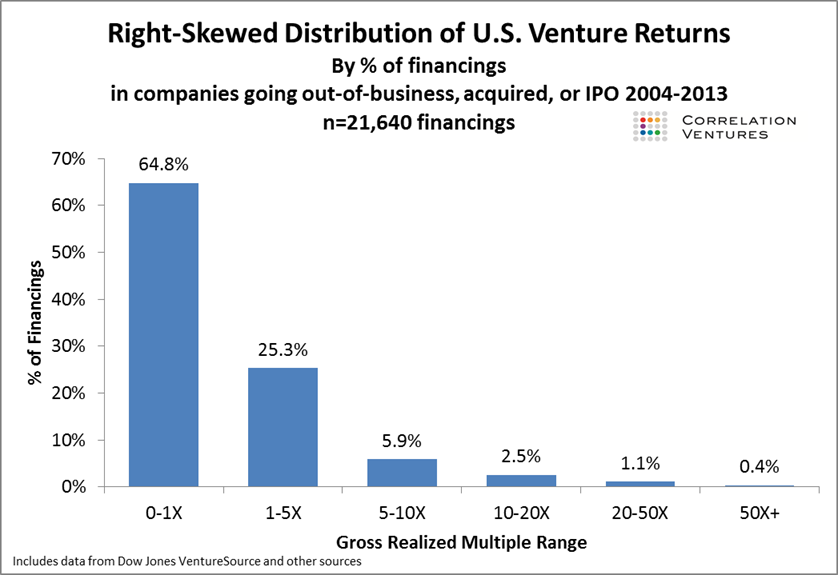

The data below from Correlation Ventures, and CBInsights is pretty self-explanatory.

Correlation Ventures’ data looks at individual financings rather than at individual companies – one company can have multiple financings. The data from CBInsights looks at individual startups, where, similarly, one startup can have multiple financings.

My conclusion, based on these two pieces of analysis, is that an early stage VC should expect that at least 50% of the startups in any given fund portfolio will lose all the money that the VC invests in them. The data from Correlation Ventures suggests an even more grim outlook – though as you’ll see later it is somewhat less categorically conclusive. However one looks at the data, the conclusion is sobering.

To put the data in context, for a while the rule of thumb was that 33% of the startups in a VC portfolio would go to zero, another 33% would return invested capital, and the remaining 33% would do significantly better – resulting in the 3x net return that limited partners expect.

Given this state of affairs, how do different VCs think about portfolio construction and portfolio management? If you are a family office, an individual, or a corporation getting into venture capital as an asset class for the first time, and if you are investing in a manager who is raising their first fund, what should you be on the lookout for? I hope this helps frame the issues worth considering. Note that the discussion documented below centered around the data from Correlation Ventures only. I have not included every response to my tweet, only those I feel contribute directly to the topic. It is possible I have missed a few replies because the thread started branching off in several directions after a while.

Eliot Durbin (@etdurbin) from Boldstart Ventures: Two nuggets of advice I got on our early funds . . . expect 20% of portfolio to drive 80% of returns. Pay attention to founders that get those 1x – 3x returns on their first rodeo, because the next will be better. Also, third, plan your percentage reserves for follow-on investments because ownership in your winners matters most.

Jerry Neumann (@ganeumann) from Neu Venture Capital: It means you have to make enough investments so that you have a decent shot at being in some of the outliers. The expected value here is at least 1.2x.

Hadley Harris (@Hadley) + Nihal Mehta (@nihalmehta) from ENIAC Ventures: The key is to build out two models. The first is a fund model with number of companies and projections about how broad/deep you follow. The second is a liquidity model to project when money will come back for recycling, and the triggers for investing past initial investable capital. Note: The process of recycling capital allows the fund to gain leverage without exposing limited partners to additional risk beyond their capital commitment.

Albert Wenger (@albertwenger) from Union Square Ventures has blogged about uncertainty for some time, and he discusses this topic in this installment – arguing that because this distribution is now well understood, valuations are being bid up significantly. This puts small funds at a disadvantage, and contributes to the phenomenon whereby VCs raise larger and larger subsequent funds. It’s a brief post. You should read it.

Chris Douvos (@cdouvos) from AHOY Capital: Here’s a thought:

- VC has always been a power law business, so big hits drive portfolio returns . . . and the big hits are getting bigger, but on the other hand, pricing going up is going to cut returns, not only of the big winners, but also of the middle OK part of the portfolio.

- Remember: Opportunity = Value – Perception, and the industry is so good at blowing up perception, but true Value is more fleeting – and, if we’re being pedantic, Value is the discounted present value of future (positive) cash flows. [My comment; The dichotomy between Value and Perception that Chris is referring to explains why the data from Correlation Ventures seems so jarring at first glance.]

- But everyone’s bought into the power law dogma, so unicorns are getting bid up, often with pricing for perfect execution, following winds, and fair seas . . . any hiccup (systematic or idiosyncratic) will lead to a lot of stranded unicorns, or as Bryce (of Indie.VC) calls them, “donkeys in party hats” . . . Speaking of which, I think his efforts over at Indie.VC have been a creative and thoughtful search for Opportunity in the context of Value – remember, Opportunity = Value – Perception.

- At the end of the day all that matters is Moolah in da Coolah – the distributed to paid-in-capital multiple that a fund ultimately achieves. Here was my effort at thinking about some of these portfolio construction issues in the context of valuation environment: All About the Benjamins.

- But I remain really nervous about the environment. As Henry McCance at Greylock told me in 2001, VC works well when time is cheap and capital expensive. When that relationship is reversed, trouble ensues.

Dave McClure (@davemcclure), formerly of 500 Startups:

- This means you should do a LOT more deals, unless you pick better than Sequoia. Of course depends on dealflow, selection, and stage, but if you start investing at seed-stage, most GPs with portfolios with N < 50 companies are playing Russian roulette. If large outliers of > 20x happen only 1% – 2% of the time, basic math would suggest a portfolio size of N > 100 is more rational.

- [My comment; Yes, The basic math certainly supports that conclusion. Though, I wonder if there are nuances the basic math doesn’t capture. Do you think there are conditions under which one might justify deviating from that prescription?] Well if you’re a subject matter expert and/or have excellent access to dealflow or an established brand, you might choose to build a concentrated portfolio – but again you’d have to convince yourself, hopefully based on data, that you’ll generate a higher percentage of outliers than the average VC.

- [My comment; Got it . . . Though, one has to wonder if there’s such a thing as a subject matter expert when it comes to predicting how the future will unfold. But, I see why that approach would make sense – in some rare cases. Who would you say does that really well? Anyone? CVCs?] Well for specific IP-related areas, people who are scientists/PhDs/professors might have an advantage. For industry verticals, maybe experienced business or technical folks. Famous people and/or famous VC firms might also have an advantage. Not sure about CVCs, unless specific IP perhaps.

- [My comment; That reminds me of one of the points Richard Zeckhauser makes in Investing in the Unknown and Unknowable; collaborate with other investors with superior knowledge of specific industry verticals, among other things.]

Josh Wolfe (@wolfejosh) from Lux Capital:

Huge wins are rare / Mostly luck / Claimed as skill / But huge wins beget halos / And halos beget better reputation / And better rep begets better opps / And better opps up the odds / That you get lucky / With a rare huge win [My comment; Josh typed this like a poem. I just couldn’t figure out how to get that layout using this new UI on WordPress. I have spent a lot of time thinking about the skill versus luck dichotomy in early stage VC. So one way to think about this discussion is to ask; In relation to portfolio construction, what can a seed-stage VC do to optimize luck?]

Tren Griffin (@trengriffin), author of 25iq – a blog about markets, tech, and everything else:

At the core of almost everything is probability. The future is a probability distribution. The best processes creates favorable odds of a correct decision. A good process can create a bad result and vice versa. Quoting Warren Buffett:

Fred Destin (@fdestin) of Stride.VC:

- In my experience the skew is almost systematically massive. With one fund returner – your fund is likely to be fine, with two – it’s likely to be great, etc. The top 2 to 4 exits will likely more than 2x+ the fund, the next 5 to 8 exits together will return 1x the fund, and the rest might lose some money.

- Hence I’m always thinking – never invest in anything that can’t return the fund – which is, of course, a function of ownership and upside, with upside uncapped if you want to have a shot at a “glimmer of greatness”.

[My comments; Thanks, Fred. “Never invest in anything that can’t return the fund.” How does one figure this out? In one of his books Nassim Nicolas Taleb talks about two forms of analysis; First – Thinking forward to the future state, and then, Second – Thinking backwards to the current state. But, how does one do that without succumbing to magical thinking? Are there other approaches? I created a grid based on a blog by Bill Gurley – All Revenue is Not Created Equal: The Keys to the 10X Revenue Club. But, I’m always wondering how others approach this question. I have to admit, team decision-making then becomes an issue . . . Doesn’t work if rest of the team doesn’t buy into systematically thinking about that question as a group. I used a similar approach to guide my effort to determine if a startup has the potential to develop moats. This also raises an issue that Dave McClure mentioned in our exchange on this same question; A VCs ability to add value – early customer introductions, engineering outcomes to help avoid or minimize the scenarios where a startup doesn’t return invested capital – makes a big difference – I noticed this while I managed a fund of funds portfolio at KEC Holdings between 2008 and 2012. I’m confident using a template or checklist is helpful – Michael Mauboussin discusses that approach in The Success Equation. A question in my mind is how Lisa and I can codify best-practices into decision-making processes as we get REFASHIOND Ventures off the ground. But perhaps as Hadley and Eliot alluded, it’s a question that requires a multi-step solution with at least 2 layers of analysis; First – a fund level macro analysis, and then, second – an analysis of each investment to see how it fits the fund level macro framework. Though, I think in Zero to One, Peter Thiel discusses how at the early-stage one differentiator is a VCs qualitative analysis of how the future will unfold more so than anything else. That does not negate anything that’s been said so far, but it suggests that there’s a lot of room for interpretation.]

- Tie decision making to absolute rules (eg I need a moat in every investment) and you’re introducing a systematic bias / hard screening criteria. That may be fine – but don’t confuse a disciplined decision-making process and method with fixed decision-making “rules”. The only rule that should be fixed in my opinion is: the potential for unlimited upside exists within the fund’s duration. [My comment; I agree. It’s less about absolute rules, and more about ensuring I have thought about the issues and have consciously decided one way or the other. I think it’s important to do that when things are uncertain and and failing to think through the issues is costly. As you point out, it’s more about process than hard rules . . . Especially – at the stage at which I’m doing this there are no moats yet, but I need to consider the possibility that they can develop over time, and why that may happen if things work out. But, point taken re systematic bias.]

Never invest in anything that can’t return the fund.

Fred Destin, Stride.VC

Note: At this point I shamelessly plugged my work on Economic Moats: Economic Moats for Early-stage Tech Startups (Half a Dozen Blog Posts & A Presentation. Also, note that there’s a philosophical divide about economic moats and startups among VCs. Some think they matter. Others do not. I think they do, and I think a careful analysis of the issue leads to that conclusion for startups that will go on to return an entire fund, for example. However, I also agree with the observation that at the the earliest stage of a startups existence the thing that matters most is the startup’s ability to make its customers happy as it conducts the search for a scaleable, repeatable, and profitable business model.

An economic moat is a structural feature of a startup’s business model that protects it from competition in the present but enhances its competitive position in the future.

This is the definition of an economic moat I have settled on, based on my work thinking about the topic from my specific vantage point as an early stage VC.

Ed Sim (@etdurbin) from Boldstart Ventures: Great questions but don’t overthink it; First, every investment has to have opportunity to return fund. Second, ownership matters. Third, reserves matter. A related question; What is your return the fund exit (RFE) for each investment assuming dilution? That analysis will show that ownership and reserves matter, and so does capital efficiency. [My comment – I have known Ed and his partner, Eliot since 2012; Ed! I am trying to find the Goldilocks Zone; not too much thinking, but not so little that we get taken by surprise . . . I agree working through these points will cover most, if not all the necessary ground.]

What is your return the fund exit (RFE) for each investment assuming dilution?

Ed Sim, Boldstart Ventures

Sean Glass (@SeanGlass), Founder and CEO – Advantia Health. Founding Partner – Acceleprise; What was the return on that meta portfolio? I think the role of vc as investor is to generate alpha, and you do that by taking an approach that gives your portfolio asymmetric risk. Just like with public equity investing there are a different approaches to doing that.

Sean’s comment raises an observation first made by, Arjun Sethi (@arjunsethi), who is Co-Founder of Tribe Capital, and formerly of Social Capital, Yahoo, and MessageMe, and LoLApps – about the graph from Correlation Ventures; The graph is a poor illustration of what defines a venture round, fund and timeline of investment. [Jerry Neumann’s comment; Agree. The data is fairly useless. If you take the bottom end of each bucket it’s 1.2x, top end (except 50x+) it’s >4x. So, runs the gamut.]

Deepak Gupta (@DeepakG606) from WEH Ventures; The Correlation Ventures data refers to financings and not number of companies. It’s possible a VC made an overall 10x+ in aggregate in one company but would still be hitting 2x or 1x fund in this data. So overall percentage of multibagger companies will be higher than suggested by this analysis. [My comment; This is true, given the modeling I have been working on. There are scenarios in which the fund would fail to meet LP expectation of a 3x+ net distributed to paid-in-capital ratio even though the percentage of big winners is non-zero. It’s quite trivial to see how this might happen if the general partners’ capital allocation decisions do not ultimately work in the fund’s favor.]

- I wouldn’t go as far as to say the data is completely useless, though I see the argument Arjun and Jerry are making. If one assumes that the two sets of data suggest possible probability distributions, then I think the interpretation should be that; First, any portfolio construction that assumes less than 50% of the portfolio going to zero is almost certainly naively over-optimistic. Second; assumptions about big winners should be scrutinized closely because they are rare – so fund managers should be able to explain how they will attract dealflow that will include more than their fair share of potential fund-returning startups AND the processes they have developed to maximize the chance that they actually select those startups for inclusion in the fund’s portfolio.

- In my work on modeling portfolio outcome scenarios for REFASHIOND Ventures’ first fund, I have gone as far as assuming 90% of the portfolio goes to zero. I have not modelled 100% of the portfolio going to zero because that’s obviously the trivial case – if that happens we’ll most certainly have bigger problems to worry about. Most of the time spent in discussions between prospective limited partners and the venture fund’s general partners should be in arriving at underlying assumptions that reflect reality and can be justified by how the general partners have said they will run the fund, with enough flexibility to allow the fund to exploit unforeseen and unexpected opportunities as they arise in real-time – remember that optimizing luck is an important aspect of all this.

- Correlation Ventures has not made public a version of this analysis that presents the results in a manner similar to that done by CBInsights. It is likely that they were unable to get to that level of granularity given the source data, or they may prefer to keep that specific version of the analysis as a trade secret.

Dan Buckstaff (@Buckstaff) shared a link to an article by Morgan Housel (@morganhousel) from Collaborative Fund – Tails, You Win; It’s a short article and you should read it if you want to learn more about how prevalent power laws are around us. I like this quote from Benedict Evans – I have paraphrased it to refer to Early-stage Venture Capital rather than Silicon Valley: Early-stage Venture Capital is a system for running experiments. It’s the nature of experiments that some fail – the key is for the ones that work to really really work. [My comment; Once you read the article you should notice that it echoes themes from the comment Josh Wolfe made earlier.]

Early-stage Venture Capital is a system for running experiments. It’s the nature of experiments that some fail – the key is for the ones that work to really really work.

Paraphrasing, Benedict Evans, Andreessen Horowitz

Baris Guzel (@BarisGSF), of BMWi Ventures, pointed me to a blog post by Seth Levine (@sether) from Foundry Group – Seth’s contribution to the discussion is below;

- To your specific question; Given skewed outcomes what’s the right strategy for a small fund? in general smaller funds will have less opportunity to consolidate ownership in outperforming companies. Thus I think the right strategy is to seek more exposure – place more bets. [My comment; Thanks, Seth. There seems to be a tension between seeking more exposure AND getting as much ownership % as early as possible, and reserving capital to follow on in later rounds. Especially, in the context of a fund 1 with say $10M – $20M of AUM. Thoughts? If you had to choose?]

- There’s definitely that tension. In an ideal world you’d have enough capital and enough early, but predictive, data to consolidate into your best companies. Larger “Series A” funds do that regularly, but with a seed fund you have challenges with both capital and information.

- You have a small fund and by the time you have to make a follow-on decision, or more ideally preempt a round, you don’t really have that much more data about the opportunity. That’s really the argument for placing as many early bets as possible.

- The ones that run on you drive value and you’ll have plenty of exposure to the potential for upside. It’s easy to say in hindsight that you “knew” something was going to be great, but how often do you have that reliable insight between Pre-seed, Seed, Seed+, and Series A? [My comment; I know that’s a rhetorical question, but there’s so much pressure to seem prescient, all knowing, and fully certain about the future . . . But yes, it’s generally hard to know. So it seems things point back to the decision-making process, and a bit of luck, as others have alluded. I’ve stopped paying attention when people tell me to “sound more confident about what you’re saying” . . . How can one be confident when decisions are being made under extreme uncertainty? I’ll stop bloviating.]

- Re: Luck, that reminded me of this ancient post of mine (2005 – I was an associate) about what makes a good venture capitalist and David Cowan’s comment, which has always stuck with me. [My comment; I couldn’t find the blog post Seth is referring to, but I found a discussion thread elsewhere in which David Cowan, of Bessemer Venture Partners says the correct answer to the question “What do you think is the most common trait among successful venture capitalists?” is “Luck.” This reminded me of a blog post I wrote about Fab.com around the time I was studying economic moats; Vcs often rail about startups raising too much money at valuations that are too high to sustain, but VCs too sometimes make investments that assume perfect knowledge, perfect execution by the team, perfect market adoption . . . etc, to the point Chris Douvos made earlier. I wonder how the early stage venture funds that invested in Fab.com have fared. I have not looked that up yet.]

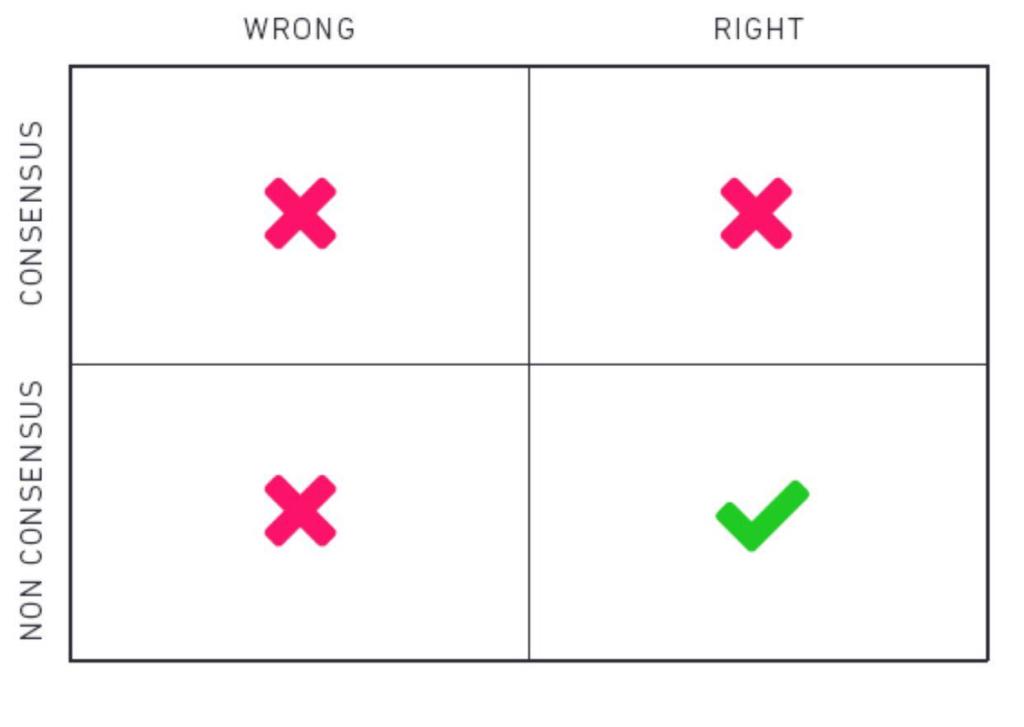

This also calls to mind a quote from Andy Rachlef, formerly of Benchmark Capital; Investment can be explained with a 2×2 matrix. On one axis you can be right or wrong. And on the other axis you can be consensus or non-consensus. Now obviously if you’re wrong you don’t make money. The only way as an investor and as an entrepreneur to make outsized returns is by being right and non-consensus.

This article by Tren Griffin delves deeper into the topic: Why Investors Must Be Contrarians to Outperform The Market.

Investment can be explained with a 2×2 matrix. On one axis you can be right or wrong. And on the other axis you can be consensus or non-consensus. Now obviously if you’re wrong you don’t make money. The only way as an investor and as an entrepreneur to make outsized returns is by being right and non-consensus.

Andy Rachlef, formerly Benchmark Capital, now at Wealthfront

Note: At a certain point in the discussion on Twitter a side-bar discussion developed about how much help seed-stage venture capitalists should provide to startups in which they have made an investment as those startups search for product-market-fit. I am not including those here as that is a separate topic worth exploring on its own.

Chinedu Enekwe (@Cope84) from Affiniti VC; Very true – risk in the winner and finding ways to coach the laggards into favorable exits. [My comment; He highlighted this blog post by Fred Wilson (@fredwilson). It’s worth reading, if you’re an emerging manager coming to grips with how to manage your portfolio. The primary uptake from Fred’s blog post is that the best early-stage VCs spend more time with startups in the second and third quartile of portfolio returns than with startups in the top quartile. This is keeping with my beliefs on the topic; The very best investments in an early-stage VC portfolio will do fine, those founders are pretty self-directed and resourceful. They will succeed with or without anyone’s help. Also, they are very proactive about letting investors know what assistance will be most beneficial to them, in advance. So where a VC can really move the needle with regard to portfolio returns is with the startups and founders that really need some help to avoid returning 0x the invested capital. I saw this play out in a fair amount of detail when I was also responsible for performance monitoring and reporting on a sizeable fund of funds portfolio between 2008 and 2012 – it included early stage VC funds, growth funds, buyout funds, hedge funds, and some public equity active funds.]

Note: The following discussions were not part of the thread that formed from my question on Twitter, but they are relevant, and so I am including them here.

Samir Kaji (@Samirkaji) from First Republic Bank; Shared an article by Clint Korver of ULU Ventures: Picking winners is a myth, but the Power Law is not. It is worth reading Clint’s article because he introduces some added dimensions to the discussion. Here’s additional advice from Samir, some of which I got over email, and then during a call with him when Lisa and I told him about REFASHIOND Ventures. I have also cherry picked comments from some blog posts he’s written on the topic.

- To maximize the probability of success, fund GPs raising a first fund should perform the portfolio construction exercise based on their investment thesis, their knowledge of the market in which they plan to operate, and how much capital they need to prove that they can execute the thesis. Although, macro considerations are always a concern for managers raising their very first fund, this exercise should be performed independent of considerations from prospective LPs who make comments such as “You should not raise more than $X for your first fund.” In other words the dog should wag its tail, not the other way around. He discusses that topic here: Is there ideal portfolio construction for seed funds?

- Although many will pejoratively speak of large portfolios as “spray and pray”, doing so ignores years of probability and statistics, and likely over-weights skill versus luck.

- That said, larger portfolios do come with some challenges: Scaling value-add to portfolio companies. Requiring larger exits (given smaller initial checks/ownership vs. concentrated portfolios) for definition of outlier (fund returner). Tougher to make follow-on decisions.

- When pitching LPs, at a minimum expect to discuss

- Target Fund Size,

- The stage at which the fund will make its initial investments; Pre-seed, Seed, Series A, Series B . . . or later,

- Average Initial Check Size,

- Average Initial Ownership Target – which establishes the valuation bands within which the fund should invest,

- Total Number of Startups in the Portfolio – a range is the norm,

- The fund’s Follow on Reserve Percentage, and

- The Fund’s Investment Period.

- As conversations progress, more sophisticated LPs may want to discuss the key assumptions driving the sort of scenario analysis I described earlier. Clint performed a simulation to arrive at the conclusions in his article.

Conclusion: The goal of this article was to develop a qualitative understanding of how other VCs think about portfolio construction and portfolio management from the perspective of an emerging early-stage VC raising an initial fund of between $10M and $25M of AUM. Limited Partners in a new manager raising a first fund face the same questions about making an investment that venture capitalists encounter when they seek to first deploy capital into a startup they have just met. For most LPs the easier decision is “wait and see” rather than to take on the uncertainty, risk, and hard work necessary to make a decision to invest in a new VC fund manager. One way to get LPs comfortable making a commitment is to;

- Demonstrate that the new manager has a unique investment thesis based on knowledge about a market that is under-appreciated by other investors,

- Demonstrate an ability to source deal-flow in a manner that is both efficient and proprietary – given the rule of thumb that the best VCs see 100 startups for every 1 investment they make,

- Demonstrate the ability to pick startups that have a high probability of returning the portfolio within the duration of the fund,

- Demonstrate an ability to manage the portfolio’s losses in a way that maximizes the likelihood that the fund will meet LPs’ expectations, and

- Demonstrate an ability to execute the fund’s stated portfolio thesis, portfolio construction and portfolio management strategy under real world scenarios.

This is by no means an easy task, and it is only one of the many issues an emerging manager raising a first fund must worry about. As has been reiterated more than once previously, it requires hard work, smarts, keeping one’s wits about oneself, and a fair bit of luck.

Additional Reading:

- By Hunter Walk from Homebrew VC: Two Portfolio Tips For First Time Seed Funds

- By Christoph Janz from Point Nine Capital: Good VCs, Bad VCs

- Jerry Neumann: Power Laws in Venture

- There’s a lot more here: #BeYourOwnMentor – Independent Study in Early Stage VC

About The Worldwide Supply Chain Federation

The Worldwide Supply Chain Federation is the collaborative, and mutually supportive coalition of open and multidisciplinary grassroots communities focused on technology and innovation in the global supply chain industry. Founded in August, 2017, The New York Supply Chain Meetup is its founding chapter. The New York Supply Chain Meetup is the world’s largest, fastest growing, and most active community on Meetup.com – with well over 1700 members. The Worldwide Supply Chain Federation is the first community of its kind to focus on supply chain, innovation, and technology. It seeks to bring together BUYERS and BUILDERS of the technology innovations that will refashion global supply chains.

About REFASHIOND Ventures

REFASHIOND Ventures is an emerging early stage venture capital firm that is being built to invest in early-stage startups creating innovations to refashion global supply chain networks. REFASHIOND Ventures is based in New York City. The Worldwide Supply Chain Federation and The New York Supply Chain Meetup are initiatives of REFASHIOND Ventures.

Update: March 23, 2019 at 08:32 to fix some mechanical errors, typos, grammar. Also added definition of a startup, and definition of an economic moat, and highlighted some quotes.

[…] Laung Aoaeh of REFASHIOND Ventures put together one of the most comprehensive docs on seed fund construction I’ve seen. While not shocking, this is a great one to bookmark and send to anyone […]