Originally published at www.refashiond.com on October 25, 2018.

By Brian Laung Aoaeh and Lisa Morales-Hellebo

Authors’ Note: This is the second in a series of six articles about problems and opportunities in global supply chains, with a focus on the fashion industry. In this article we focus on trying to learn how executives at fashion industry incumbents may learn how to predict technological disruption in order to develop appropriate responses to the evolving environment that surrounds their companies. We start by briefly surveying some of the theory about disruption. Then, we delve into a series of brief historical analyses of technological disruptions in a number of industries. We try to understand those episodes by using the theoretical foundations developed earlier. Finally we ask the question that forms the basis for this article, by posing questions about potential sources of disruption in the global fashion industry, the issues that every team of c-level executives in the industry worries about daily. If you have not read the first article in the series you may do so using this link: The Fashion Supply Chain Is Broken. However, reading the first article is not a prerequisite for following this discussion.

Acknowledgement: We are grateful to Tayo Akinyemi for reading and critiquing previous versions of this article.

The fashion supply chain is broken and must be refashioned. This is the conclusion we have come to after studying the issue, starting in 2014.

Background

We each independently became interested in supply chains in 2014. We have collaborated with one another in learning about supply chain since June 2016. In August 2017 we teamed up to start The New York Supply Chain Meetup, and building on that work are on the verge of launching The Worldwide Supply Chain Federation when The Bangalore Supply Chain Meetup hosts its kickoff event in November. In September 2018, we teamed up to start building REFASHIOND: a venture firm that will invest in early-stage startups creating innovations that make global supply chains more efficient. We will initially focus on startups at the intersection of fashion and retail. You can learn more about us by visiting REFASHIOND’s website. We also provide more detail about our background in the first article in this series.

In order to ensure that everyone is on the same page about disruption, we have chosen to conduct a brief survey of the key ideas that underpin the concept. We believe this is necessary to ensure that any dialogue that ensues is on the basis of a shared mental model. In writing this article we took inspiration from the work of Joshua Gans, author of “The Innovation Dilemma.” His work has greatly helped our understanding of innovation and disruption theory.

We do not claim to have a special talent for predicting disruption, however Lisa has a track record of leading disruptive innovations and has been featured in the book, “Disrupters: Success Strategies from Women Who Break the Mold.” This is not an article in which we are going to provide canned answers. Rather, our focus in writing this article is two-pronged: First, we will briefly examine the theory behind disruption, and attempt to connect the dots between various schools of thought on the subject. Second, using the lessons from that exercise, we will then look at some historical examples of disruption and see what insights we might glean from them.[1] We conclude the article by considering where disruption in the fashion industry may come from.

Our goal is to foster and participate actively in industry-wide dialogue about the future of the global fashion industry. We hope the result of such dialogue will be inter-industry collaboration aimed at making the future reality more prosperous and sustainable than the present or the past. We’re excited about participating in such conversations with startup founders and fashion industry executives.

Do not hesitate to email us if you would like to speak with us about our work, and possible collaborations in the future.

We can be reached at:

- Lisa Morales-Hellebo — lisa@refashiond.com, and

- Brian Laung Aoaeh — brian@refashiond.com.

What Is Disruption?[2]

Creative Destruction — A Result of Fundamental Market Shifts

Joseph Schumpeter (1883–1950) is the first person to have clearly described the concept on which subsequent work on developing a theory of disruption is based.[3] He describes “Creative Destruction” as:

“The opening up of new markets, foreign or domestic, and the organizational development from the craft shop to such concerns as U.S. Steel illustrate the same process of industrial mutation — if I may use that biological term — that incessantly revolutionizes the economic structure from within, incessantly destroying the old one, incessantly creating a new one. This process of Creative Destruction is the essential fact about capitalism.”

He goes on to say that Creative Destruction is about more than price competition:

“But in capitalist reality as distinguished from its textbook picture, it is not that kind of competition which counts but the competition from the new commodity, the new technology, the new source of supply, the new type of organization (the largest-scale unit of control for instance) — competition which commands a decisive cost or quality advantage and which strikes not at the margins of the profits and the outputs of the existing firms but at their foundations and their very lives. This kind of competition is as much more effective than the other as a bombardment is in comparison with forcing a door, and so much more important that it becomes a matter of comparative indifference whether competition in the ordinary sense functions more or less promptly; the powerful lever that in the long run expands output and brings down prices is in any case made of other stuff.”

Finally, he makes the observation that:

“The fundamental impulse that sets and keeps the capitalist engine in motion comes from the new consumers’ goods, the new methods of production or transportation, the new markets, the new forms of industrial organization that capitalist enterprise creates.”

Disruption — A Result Of Movement Up The Technology S Curve

Richard Foster examined the role that technology plays in disruption, and used technology S curves to advance our understanding of disruption in his 1986 book, “Innovation: The Attacker’s Advantage.” An S curve is a graph of a logistic growth process. In such a process, growth is initially slow, speeds up in the middle period, and then levels off after that, as it approaches some upper maximum limit at the end of the growth period. Foster’s key realization was that technological innovations can result in a change in the underlying process, leading to a fundamentally new S curve with a discontinuity between the original S curve and the new S curve. Using this formulation, disruption happens during the shift in customer demand from the products along the old S curve trajectory to those products along the new S curve trajectory. On a long enough time-horizon, it should be easy to understand that an industry may experience multiple waves of disruption depending on the rate of technological advancement and entrepreneurial innovation within the industry.[4]

Disruptive Innovation — S Curves & Discontinuities in Market Structure

Clayton Christensen pushed our understanding of disruption further with the publication of “The Innovator’s Dilemma: When New technologies Cause Great Firms to Fail.” Below, we highlight and summarize some of the main ideas.[5]

A Sustaining Innovation: leads to product improvements without fundamentally changing the underlying structures of the market to which it applies; it enables the same set of market competitors to serve the same customer base, while typically extracting more value from them. It is important to note that sustaining innovations may lead to a rearrangement of the competitive landscape, but rarely will they lead to the outright failure of a leading incumbent. Sustaining innovations can be radical, revolutionary, or discontinuous if they lead to dramatic and unexpected product improvement. In Foster’s formulation, a sustaining innovation merely advances a technology up the same S curve.

A Disruptive Innovation: starts out with worse product performance relative to the available alternative from market incumbents, and is often not very complex technologically. As a result the new product is attractive to a small niche of the customer base. However, if product performance improves quickly enough, at a certain point the new product provides superior product performance relative to the alternative that is available from market incumbents. This process leads to a significant, dramatic, and fundamental shift in market structure, that is to say, suddenly the new entrants go from serving a niche customer base to gaining a majority of the market while, at best, erstwhile incumbents become mere shells of their former selves or even go out of business entirely. To use Foster’s formulation, a disruptive innovation moves the product to a new S curve.

Clayton Christensen also differentiates a low-end disruption from a new-market disruption. In a low-end disruption, the attacker enters the market with a product that is inferior relative to the needs of mainstream customers. In a new-market disruption the attacker enters the market by serving a customer niche that was previously unserved by the existing incumbents.[6] A low-end disruption results from a low-end innovation while a new-market disruption is the result of a new-market innovation.

Architectural Innovation — A Fundamental Change in Systems

Rebecca Henderson and her co-author, Kim Clark, focus on another important component that adds to our understanding of disruption: Why is it so difficult for incumbent firms to respond even when they possess the technical expertise to do so? In “Architectural Innovation: The Reconfiguration of Existing Product Technologies and the Failure of Established Firms,”[7] they make the distinction between the components that are combined to form a product and the system that makes it possible to combine disparate components into a single product or a unified service offering.

Component Innovation: is innovation in the modular design of a product. Such innovations are easy for incumbents to respond to because they arise from using technical knowledge about each component of a product to make improvements to the overall product, within existing organization structures and business models. Component innovation arises from component knowledge.

Architectural Innovation: is innovation in the end-to-end system that enables the combination of various, disparate components to form a product. Incumbent firms find it difficult to adapt to such innovations because the innovations render the incumbent’s component knowledge useless, given that the innovation is in a new organizational structure or a new business model that reconfigures the end-to-end system leading to the creation of a product using the same core body of component knowledge. Architectural innovation arises from architectural knowledge.

A key observation in Henderson and Clark’s work is that a market disruption — the attacking new entrant quickly supplants the incumbent in terms of market share and market power, leading to financial distress for the incumbent, can occur in a market when a sustaining innovation is married with architectural innovation. This helps explain certain market disruptions that would not qualify as disruptions if we only used the Christensen formulation.

Technology, Innovation, and Disruption — Two Sides To The Story

Joshua Gans helps us connect the dots more fully between Clayton Christensen’s Disruptive Innovation and Rebecca Henderson and Kim Clark’s Architectural Innovation. In “The Disruption Dilemma” he introduces us to the concept of a Demand-Side Disruption and Supply-Side Disruption. Below, we explore those ideas in more depth.[8]

The Demand-Side Theory of Disruption is an outgrowth of the Christensen School, wherein as attackers enter a new market incumbent firms perform a demand-based risk assessment and decide that mainstream customers are highly unlikely to desire the product on offer from the attackers. In fact, in many cases, the appearance of such inferior products is welcome because unprofitable customers move to adopt the products now being offered by the upstart attackers, freeing incumbents to focus all their resources on their most profitable customers. This is all well and good, until, through the process of iterative improvement, the attacker’s product moves rapidly up the new technology S Curve and quickly achieves performance-parity with the incumbents’ product at a significantly more attractive price-point. It is at this stage that customers abandon the incumbent in favor of the attacking firm in cascading waves, causing seemingly sudden failures of once dominant incumbent firms. This is a vast simplification of the discussion by Gans, however the key to understanding demand-side disruption is that it is driven by changing consumer tastes and expectations.[b]

The key to understanding demand-side disruption is that it is driven by changing consumer tastes and expectations.

The Supply-Side Theory of Disruption is an outgrowth of the Henderson-Clark School, wherein as attackers enter the market it becomes extremely difficult for incumbents to respond because the basis on which they have achieved success attaches them to a certain foundation of architectural knowledge from which they cannot detach themselves even if they admit that that their core business is at risk. To respond, incumbents must develop an entirely new system of doing things. This is difficult for incumbents to do since, at the outset, there is no guarantee that the new system will succeed any better than the existing architecture which has been the basis of the incumbent’s historical success. In other words, uncertainty causes incumbents to drag their feet about making the difficult choices they must make in order to adapt, assuming they know what changes need to be made. Remember that the architectural knowledge which forms the basis on which attackers enter the market is invisible to incumbents, and the attendant uncertainty makes an already daunting task even more difficult.[c]

The architectural knowledge which forms the basis on which attackers enter the market is invisible to incumbents, and the attendant uncertainty makes an already daunting task even more difficult.

So What?

Now that we have surveyed some of the key ideas in disruption theory, we’ll explore how disruption has played out in a few industries. Before we do so, it is worthwhile to reconcile the ideas we have encountered in the preceding discussion.

First, if emerging technologies progress quickly enough up the technology S Curve and gain sufficient customer adoption, the probability that a disruptive event will occur in a given industry increases until it becomes practically inevitable. This evolution is accompanied by a high degree of uncertainty about future states of the world. The uncertainty complicates decision-making for the executives who must decide how incumbent firms should react when attackers enter the market with a low-end or new-market offering.

Second, architectural innovation will always lead to a degree of market disruption if it catches a wave of changing and favorable consumer expectations. A sustaining innovation that is combined with architectural innovation will lead to an outcome to which incumbents cannot respond even though they possess the technical knowledge to respond to the component-level innovations. Since architectural knowledge is invisible, there is no way for incumbent’s and other competitors to respond to architectural innovation without assuming risks of an existential nature given that they have no real understanding about how the innovation works, assuming they recognize and admit there’s an innovation before it is too late.

A disruptive innovation married with architectural innovation will lead to potentially more extreme market dislocations because incumbents can only respond to the component-level innovation on the basis of old architectural knowledge. This will cause their offerings to consistently underperform the products introduced by the attacking firms along the dimensions that now matter most to customers. Eventually waves of customers will abandon the incumbent product in favor of the new product offered by attacking new entrant firms. In other words, the new architecture supplants the old.

Third, the forms of innovation we have discussed above are not mutually exclusive. Rather, it is often the case that each form of innovation is present to a certain degree in any case of market disruption that one studies

Fourth, and this bears repeating, it is a mistake to ignore the role that uncertainty plays in complicating the decision-making process that individuals in positions of authority within incumbent firms face.Uncertainty is the factor that causes decision-paralysis, buying attackers time to gain strength and ultimately dislodge once powerful incumbents.

Uncertainty is the factor that causes decision-paralysis, buying attackers time to gain strength and ultimately dislodge once powerful incumbents.

Does this sound frightening? It is. Why? It means that, on average, chief executives, chief technology officers, chief strategists, heads of innovation, and other senior executives, are altogether incapable of protecting leading incumbent firms from failure. Not unless the entire firm adopts a culture whose strategic choices are informed by assessments of demand-side and supply-side innovations. Even then, as Schumpeter observed, it’s just a matter of time before every incumbent is overwhelmed by waves of creative destruction. To a certain extent, this may explain why over the course of the recent past, companies that continue to be led by members of the founding team demonstrate a greater capacity to cause and respond to potential market disruptions than incumbents managed by teams of professional executive managers who did not found the company.[9]

We now turn our attention to some historical examples of disruption. For brevity’s sake, we have intentionally left out many details.

Disruption In Action

Tech Ate Books

Between 1960 and 1970 mall-based chain bookstores started supplanting independent bookstores. This process continued till about 1980, when mall-based chain bookstores suffered a similar fate with the rise of big-box bookstore chains. By 2000 big-box chains like Barnes & Noble, and Borders dominated the market. However, with the advent of the internet and its adoption for online retail; Borders is already out of business, while Barnes & Noble is struggling to reorganize and sustain its business.

We believe this is an example in which architectural innovation is the dominant factor at play. However, one should not underestimate the contribution of changes in consumer behavior. As our teenage and pre-teen children remind us; “Amazon’s supply chain is so awesome! You do not have to go anywhere, they will just bring your stuff to you while you stay home and play video games.” As time has progressed and digital media technology that is delivered over the internet has improved, disruptive innovation has come increasingly to the fore as ebooks and audiobooks began gaining in popularity.[10]

Tech Ate Video

Film projection technology started to become available between 1900 and 1930. As the technology matured, the period between 1930 and 1950 came to represent the Golden Age of Hollywood. Between 1950 and 1960, broadcast TV, small screen, and videotape recording gained a foothold in the market. The three decades between 1960 and 1990 saw the proliferation of color TV, and home video recorders. Notably, Blockbuster was founded in 1985. From 1990 to 2000 flat screen TVs, laser discs, and video CDs appeared as technologies in this market. Netflix was founded in 1997. Between 2000 and 2010, DVDs and mobile viewing become more mainstream. Netflix expanded its DVD rental business by introducing an over-the-top (OTT) streaming option in 2007. Since 2010, Video-Over Internet Protocol (Video-Over IP) and OTT video have gained dominance in terms of consumer consumption of video content. Blockbuster filed for bankruptcy protection in 2010, eventually becoming part of DISH Network which acquired the assets of Blockbuster in a bankruptcy auction in 2011. In 2013, DISH announced that it would close all of Blockbuster’s store and DVD-by-mail operations in early 2014. Meanwhile, Netflix is now available in 190 countries with 130.1 million paid subscribers and 137.1 million subscribers overall. Netflix generated more than $11 billion in global revenues in 2017.[11]

Once again, from the perspective of an incumbent’s chief strategist, or a head of innovation worried about protecting the incumbent from disruption, a more complete explanation of the circumstances that surrounded this episode can only be found by combining the Christensen School’s Theory of Disruptive Innovation with the Henderson-Clark School’s Theory of Architectural Innovation.

At the outset, Netflix entered the market with an architectural innovation: Blockbuster was not designed around a system of mailing videotapes or DVDs to people’s homes. As internet technology matured and broadband connections to people’s homes became ubiquitous, the low-end innovation of streaming video provided the final punch required to send Blockbuster crashing to the proverbial canvas of bankruptcy court. As OTT and Video-Over IP technology travelled up the technology S-Curve, Netflix had the advantage of far less in overhead costs than Blockbuster, allowing it to invest more aggressively in streaming technology, and winning the market.

Tech Ate Music Stores

The Acoustic Era stretched from 1877 to 1925. During this period the phonograph and the theremin resulted from experiments in sound recording and the technology started being applied to recording music. This was followed by The Electrical Era, when electrically recorded LP records supplanted acoustic phonographs. It extended from 1925 to 1945. Between 1945 and 1975, The Magnetic Era, magnetic 8-Track Tapes and cassette tapes supplanted LP records and other electrically recorded media. The Magnetic Era was followed by The Digital Era, between 1975 and 1993. It is during this period that MP3s started supplanting magnetic tapes and LPs. The Streaming Era started around 1993 and extends till today, MP3s lead to an explosion in peer-to-peer (p2P) file-sharing platforms. These platforms have supplanted old ways of packaging and selling music, and physical music stores have now largely been replaced by online streaming services.[12]

Although, it is popular to assume that the music industry was disrupted by MP3 technology, it is not so clear to us that such a sweeping statement captures the nuance of the situation. It is certainly true that music stores as a channel of distribution for the music industry have succumbed to digital formats and channels. It is also true that sales of physical albums have plummeted as the Streaming Era has progressed. However, Warner Music Group, Universal Music Group, and Sony Corporation together control more than 70% of the market. As a result streaming platforms like Spotify, Pandora, and Soundcloud are subject to the pricing power of the big music companies. Apple’s iTunes, Amazon’s Music, and Google’s Play are somewhat protected from the supplier power wielded by the music companies because of the power that is in turn wielded by Apple, Amazon, and Google respectively.[13]

Tech Ate Phones

The history of telephony dates as far back as 1876, when Alexander Graham Bell placed the first phone call. Early advances in telephony were made by the U.S. Army Signal Corps Engineering Laboratories, Motorola, Bell System, and Ericson between 1915 and 1956. By 1956, Bell Labs had begun work on conference calling systems, and in 1964, the first video conference call was made between New York and California using a Bell Labs Picturephone. Phones began to get lighter, but they still weighed 20 pounds or more. The first mobile phone call was made in 1973 using a Motorola DynaTac prototype which weighed 2.5 pounds. The technology continued to mature after 1973, with notable developments in 1989 when Motorola introduced the MicroTac, the world’s first flip phone.

In 1992, Motorola introduced the 3200, a hand-sized digital mobile phone that used GSM technology. That was followed in 1993 by the IBM Simon, arguably the world’s first smartphone, with a pager, a fax machine, a PDA, a calendar, an address book, a calculator, a notepad, email, games, a touchscreen, and a QWERTY keyboard all included in the same mobile phone. In 1997, Nokia kickstarted the smartphone era with the Nokia 9000 Communicator. Nokia continued to improve on its phones with the 8810 in 1998, and the 3210 in 1999 — selling over 160 million units. The Nokia 7110 introduced web access to mobile phones, and GeoSentric brought GPS navigation to mobile phones. Sharp introduced the J-SH04 in 2000 — it was the first camera phone. In 2002, the Sanyo 5300 became the first camera phone to be sold in North America. Also in 2002, RIM introduced the BlackBerry 5810, it was the first device to combine a mobile phone with a data-only device that targeted white-collar professionals. Mobile phone technology kept improving incrementally, with Nokia, RIM, and Motorola featuring as dominant incumbents in the North American Market.

Apple introduced the iPhone in 2007. Google introduced its Android OS for smartphones in 2008.[14] Since then Apple’s iOS and Google’s Android OS have gone on to dominate market share in the mobile phone OS market. Apple, Samsung, Huawei, Xiaomi, and OPPO occupy the top 5 spots in terms of smartphone shipments and market share as of the fourth quarter of 2017, according to IDC Worldwide.[15] Nokia sold its mobile phone business to Microsoft in 2014 and has instead shifted into telecommunications infrastructure and network equipment manufacturing. Motorola was bought by Google in 2012 and then sold to Lenovo in 2014. RIM has ceased manufacturing mobile phones and is now focused on developing software.

Is the iPhone disruptive? Clayton Christensen did not think so in 2006, 2007, or even in 2012. Is Android OS disruptive? From the outside looking in, it appeared that the iPhone + iOS, and Android OS represented sustaining innovations based on the Christensen School, or component innovations only, based on the Henderson-Clark School.

But, what was really happening? First Apple and Google shifted the focus away from being entirely focused on hardware engineering as a source of competitive differentiation and moved the focus more towards software platforms as the source of competitive advantage. Second, this shift coincided with a growing desire from consumers for mobile devices that performed more functions than Nokia, RIM, Motorola, and the other incumbents in the market at the time offered on their mobile devices. It is generally difficult for firms that grew to prominence on the basis of skill in hardware engineering disciplines to adjust to a market where skill in software engineering forms the basis for survival.

Tech Ate Cameras

The history of cameras and photography goes farther back in history than one would ordinarily think. Although the historical details are useful,[16] we will skip the vast majority of them up to the point in 1884 and 1888 when George Eastman patented photographic film, and the Kodak roll-film camera respectively. Edwin Land launched the Polaroid camera in 1948. Eventually Kodak, Agfa-Gevaert, and Fujifilm dominated the market for analog photography and camera equipment.[17] The market for analog cameras and photography was characterized by very complex and advanced manufacturing processes, and high barriers to entry, enabling Kodak and its peers to build highly profitable consumer franchises on the basis of that technology.

Ideas and concepts related to digital photography first appeared in the early 1960s and 1970s. In 1975, an engineer at Kodak invented and built the first digital camera. Digital Single-Lens Reflex (DSLR) cameras appeared on the market in the 1980s and 1990s, and had supplanted analog film cameras by the mid-2000s. In 2000, Sharp introduced the first mobile phone that incorporated a digital camera. Now every smartphone has an integrated digital camera.

Polaroid, Agfa and Kodak filed for bankruptcy in 2001, 2005 and 2012, respectively. Meanwhile, Fujifilm continues to record some of the most profitable years in the company’s history. What gives?

Most analyses about Kodak’s fate focus on explanations based on the Christensen School of Innovation. Others assume that executives at Kodak sought to protect its photographic film and analog camera business, the company’s cash cow. However, in “The Real Lessons From Kodak’s Decline”, Willy Shih points out that such arguments mischaracterize what was really happening within the company.[18] He arrived at Kodak in 1997, and ran a division of the company charged with exploring how Kodak might exploit the opportunity presented by digital photography.[19]

The shift from analog to digital photography posed challenges on many levels. First, there were dramatic shifts in the technology of photography. Second, the nature of the technological shifts lowered barriers to entry and significantly increased the scope of the competitive landscape. Third, as a result of these shifts in the market, Kodak’s legacy business, once the source of its unrivaled dominance, now became an albatross around its neck, imposing a severe handicap from which it could not very easily escape to contend with the horde of attackers. Fourth, these changes introduced a shift in the balance of power between the players in the market, weakening Kodak’s hand while strengthening that of its ecosystem partners and counterparts.

How did Fujifilm navigate this crisis? This is the focus of Shigetaka Komori’s book: “Innovating out of Crisis: How Fujifilm Survived (and Thrived) as Its Core Business Was Vanishing.”[20] Mr. Komori is CEO of Fujifilm. In reading the book, it becomes clear that Fujifilm is alive today because it accomplished the rare feat of adjusting its business to account for both the demand-side (disruptive) and supply-side (architectural) innovations that were taking place in the global camera and photography market. Fujifilm developed three strategies to help it contend with the coming digital era: First, Fujifilm invented original digital technology of its own — it affirmatively chose to adjust and adapt to the unfolding architectural innovation. Second, the company extended the life of its analog photography business by developing innovations to increase the gap between its existing analog products and the attacking wave of early digital alternatives — responding to disruptive innovations by building sustaining innovations to buy itself some time for its efforts in adapting to the new architectural innovations to bear fruit. Third, recognizing that the digital photography business would impose low margins on the market overall, it developed new businesses that were peripheral to its analog and digital photography businesses, but that could command high margins — though, some of these businesses were sold as revenues and profits from the analog business deceptively continued to rise and show strength. Quoting Mr. Komori;

No matter how good business is, you have to foresee and prepare for a coming crisis. Looking directly at reality, you have to recognize what is happening at the moment, as well as what is going to happen in the future. You have to read the situation, understand it, think about it, and decide what needs to be done. This is what management is all about.

Tech Is Eating Tech

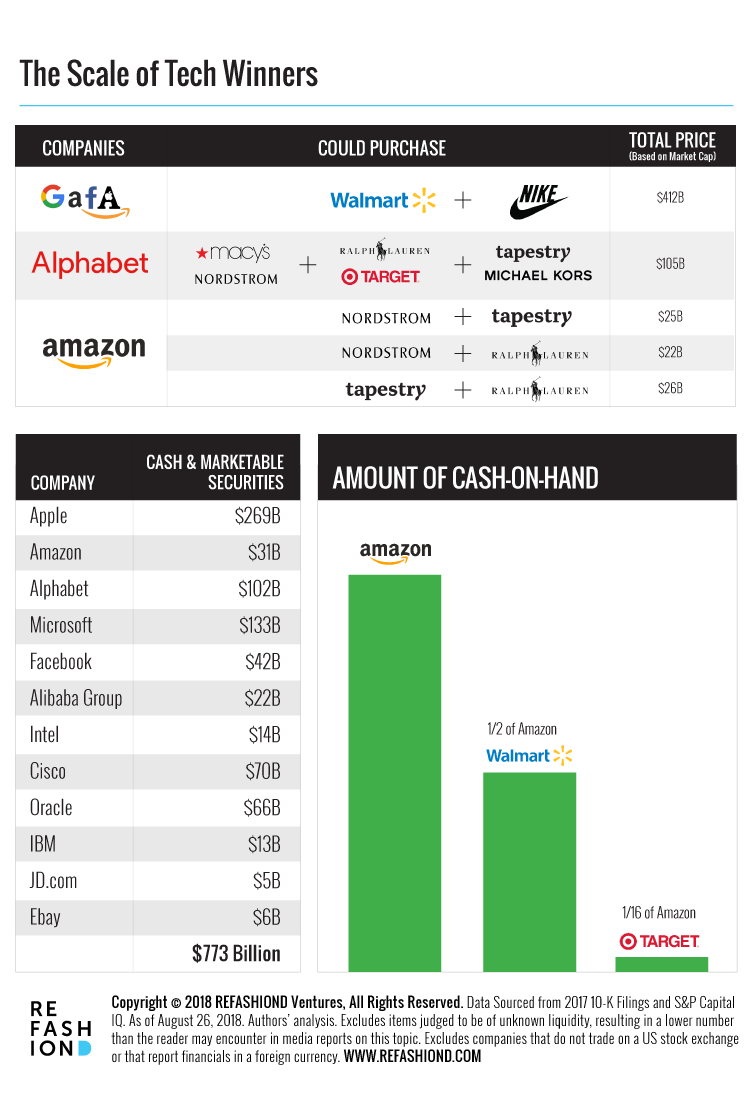

In “The Scale of Tech Winners”, Benedict Evans discusses how Google, Apple, Facebook, and Amazon have supplanted the companies that defined the the preceding technology era which was characterized by the partnership between Microsoft and Intel, and IBM to some extent. Here are some quotations from that blog post:[21]

1. “So, the four leading tech companies of the current cycle (outside China), Google, Apple, Facebook and Amazon, or ‘GAFA’, have together over three times the revenue of Microsoft and Intel combined (‘Wintel’, the dominant partnership of the previous cycle), and close to six times that of IBM. They have far more employees, and they invest far more.”

2. “Scale means these companies can do a lot more. They can make smart speakers and watches and VR and glasses, they can commission their own microchips, and they can think about upending the $1.2tr car industry. They can pay more than many established players for content — in the past, tech companies always talked about buying premium TV shows but didn’t actually have the cash, but now it’s part of the marketing budget. Some of these things are a lot cheaper to do than in the past (smart speakers[22], for example, are just commodity smartphone components), but not all of them are, and the ability to do so many large experimental projects, as side-projects, without betting the company, is a consequence of this scale, and headcount.”

3. “Google, Facebook, and Amazon are still controlled by their founders, and they are aggressive street fighters.”

In Essence, Ben is saying that no industry that offers attractive enough margins is immune from the attentions of large tech companies with ambitions of global domination. Or, as Jeff Bezos of Amazon puts it;

Your margin is my opportunity.

What Factors Lead To Market Disruption?

When an attacker emerges with a new design concept, it is rational for incumbents to ignore it, since it is uncertain whether the new design concept will gain overall market acceptance. Moreover, evidence may suggest that mainstream customers do not value the new product that the attacker is introducing to the market. This is true, up until the point at which the new design introduced by the attacker wins the allegiance of customers and other parties in the market — in effect making the new design the dominant design. In the process the design standards on which incumbents built their businesses become obsolete, and incumbents now need to adjust to a fundamentally new and unfamiliar basis of competition. It is at this inflection point that attackers start to pull away from, or catch up with, incumbents with such speed that it is rare for any of the incumbents to recover, or protect, a position of dominance.[23]

As incumbents struggle to adjust to the new paradigm, their efforts fall short of customer expectations because they may have component knowledge, but insufficient architectural knowledge to enable them to build products that meet the entirely new performance thresholds established by the attacking firms. In the examples we have discussed above;

- Ecommerce has become the dominant distribution channel for book retail.

- OTT and video-over IP has become the dominant distribution channel for video content.

- Streaming platforms have become the dominant distribution channel for people who wish to buy and consume music.

- Mobile phones now function as small computers, with software design being as important, if not more important, than hardware engineering. Moreover, despite the ridicule that mobile phone industry executives first showered on the iPhone after its initial launch, the design it introduced in 2007 now dominates the market.

- A smartphone that incorporates a digital camera has become the dominant design for the consumer photography market with further differentiation arising from computational photography, building on the strengths both Apple and Google possess in software engineering.

- Finally, technology companies that embraced the internet as a platform for their business models are supplanting those technology companies that were slow to recognize the internet’s promise.

Conclusion: Will Tech Eat Fashion?

Yes. It is just a matter of time. We believe that the global fashion industry is approaching a tipping point that is similar to one of those we described in the preceding examples. Consumer perceptions and expectations in the major fashion markets of Western Europe and North America are slowly beginning to favor speed, customization or personalization, and environmental sustainability, over lowest price. These are issues we have already touched on in the article preceding this one, and that we will discuss again in a subsequent article, so we will not belabor the point here.

It would seem that the most obvious threat comes from digital native marketplaces like Alibaba, Amazon, Asos, Farfetch, JD.com, and Yoox Net-A-Porter Group. The next most obvious potential source of danger are the vertically integrated digital native brands like Bonobos, Boohoo, Eloqui, eShakti, Everlane, Fame Partners, Forever 21, Lesara, ModCloth, Outdoor Voices, and Reformation. Another obvious potential source of threat is sharing economy and recommerce digital native companies and startups like Ebay, Gwynnie Bee, LePrix, Material World, Rent The Runway, and ThredUp.[24]

Uncertainty stems from sources one least expects. So, we decided to analyse the financial statements of the tech companies, to see what we would find. We have been surprised by how much cash they carry on their books. Leading us to conclude that tech incumbents have the cash, knowhow, appetite for risk, and other resources to initiate experiments in any industry they determine provides attractive opportunities. Along those lines we have been asking ourselves many questions, here are a couple — note we do not know if these are the right questions, but we have to start somewhere:

- Could the global fashion and accessories market attract the interest of companies whose core competence is building and deploying general-purpose software technology platforms[25]? If it did, how might that play out over time?

- Are the technologies on which global fashion industry supply chains run at risk of becoming modularized into interchangeable and rapidly evolving components? What impact will that have on the specialized knowledge that current fashion industry incumbents have accumulated? Will it make that knowledge more valuable or less valuable? How will that affect profit margins?

- How will legacy assets enable or hinder fashion industry incumbents’ ability to respond to demand-side or supply-side disruption?

- How will the competitive landscape shift if fashion industry incumbents come under increased and sustained attack from digital native competitors? This is already happening and the large incumbents — digital immigrants, are responding by acquiring digital native brands. It remains to be seen if this will enable or hinder the acquired companies’ once they become attached to incumbents. How will these digital native brands be integrated into an existing incumbents’ culture, systems, and marketing strategies?

- In what ways will concerns and awareness about climate change, and environmentally sustainable supply chains impact how the fashion industry evolves over the next decade or two? Can the industry approach this proactively?

- Is there anything fashion incumbents can do beyond iterative improvements to their existing supply chains? Circularity, customization, and localization require an entirely new supply chain architecture. How will incumbents adapt? How should they adapt? The MacArthur Foundation is doing a lot of work on this topic through its Make Fashion Circular initiative. We refer to that shortly.

The Role of Leadership

After we published the first article in this series, we received some comments from people who read the article. The following comment comes from Steve Hochman. Steve was chief operating officer at Bolt Threads from April 2017 till September 2018 after serving as an executive at Nike for over nine years. Bolt Threads harnesses proteins found in nature to create fibers and fabrics with both practical and revolutionary uses, starting with spider silk. Here’s Steve’s comment:

“Nice post today. A few thoughts: It seems there’s growing consensus that speed and flexibility is key to brands’ and suppliers’ survival and much more inter-enterprise collaboration is needed to achieve it. Thanks to Zara and others, that’s an increasingly visible insight. The harder question to me is about the leadership required to make it happen. Who will emerge to make it safe to behave this way, ie to drive and choreograph the necessary confidence and trust between historically adversarial members of the same ecosystem, and what are the first moves that will bridge us from old to new? Would love to see us explore that question, because all the technology and process investment in the world is for naught without that other answer first, I think! Thanks again for pushing the dialogue.”[26]

Steve’s comment reflects our beliefs. As Fujifilm demonstrates, proactive leadership makes it more likely that entrenched incumbents can predict and react quickly to impending market disruptions. Indeed, that is the topic of Clayton Christensen’s most recent book, “Competing Against Luck.” To paraphrase his words: Fashion industry incumbents must proactively decide that surviving market disruptions is not something they can afford to approach with a hit-or-miss attitude. Rather, they must proactively choose to predict what demand-side or supply-side innovations have a potential to disrupt their business, and then act to ensure they are among the beneficiaries of these developments. As Andy Grove, former CEO of Intel put it: “Only the paranoid survive.”

Taking control of uncertainty is the fundamental leadership challenge of our time.

– Ram Charan, The Attacker’s Advantage

We are in full agreement with the following statement from The Ellen MacArthur Foundation’s report: “A New Textiles Economy: Redesigning Fashion’s Future.”

“Transforming the industry to usher in a new textiles economy requires system-level change with an unprecedented degree of commitment, collaboration, and innovation. Existing activities focused on sustainability or partial aspects of the circular economy should be complemented by a concerted, global approach that matches the scale of the opportunity. Such an approach would rally key industry players and other stakeholders behind the objective of a new textiles economy, set ambitious joint commitments, kick-start cross-value chain demonstrator projects, and orchestrate and reinforce complementary initiatives. Maximising the potential for success would require establishing a coordinating vehicle that guarantees alignment and the pace of delivery necessary.”[27]

Transforming the industry to usher in a new textiles economy requires system-level change with an unprecedented degree of commitment, collaboration, and innovation.

We believe it is the responsibility of leaders within the global fashion industry to strive to understand the causal mechanisms of disruption, and to ask the questions that lead them towards answers that enable their respective companies to successfully navigate the waves of creative destruction that characterize capitalist economies. This is a dialogue in which we are eager to participate as early stage venture capitalists investing in supply chain startups, and as thought partners working with executives in the global fashion industry.

Next in the series: What Are The Established and Emerging Business Models in The Global Fashion Industry Today?

About REFASHIOND Ventures: REFASHIOND Ventures is an early-stage venture capital investment firm that is being formed to invest in early-stage startups creating innovations that make global supply chains more efficient, starting with startups at the intersection of fashion and retail.

About REFASHIOND CO:LAB: REFASHIOND CO:LAB is the systems design, research, and strategy consulting arm of REFASHIOND Ventures. REFASHIOND CO:LAB helps organizations create competitive advantage through supply chain innovation.

About The Worldwide Supply Chain Federation: The Worldwide Supply Chain Federation is the collaborative, and mutually supportive coalition of grassroots communities focused on technology and innovation in the global supply chain industry. The New York Supply Chain Meetup is its founding chapter.

________________

[1] We realize there’s a great risk of hindsight bias. However, analyses of this sort is one of the best tools in chief executive officers’, chief strategists’, or chief innovation officers’ toolkits and we feel it would be foolish not to use it if it helps us develop a good theoretical framework for correctly predicting, reacting to, and exploiting new innovations that threaten to reorder an industry.

[2] This discussion builds on Aoaeh, Brian Laung. “Notes on Strategy; Where Does Disruption Come From?” Innovation Footprints, 19 July 2015. innovationfootprints.com/notes-on-strategy-where-does-disruption-come-from/.

[3] Schumpeter, Joseph Alois. Capitalism, Socialism and Democracy. Routledge, 1994. Chapter VII

[4] Foster, Richard N. Innovation the Attacker’s Advantage. Summit Books, 1986.

[5] Christensen, Clayton M. Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail (Management of Innovation and Change Series). Harvard Business Review, 1997.

[6] The Innovator’s Solution: Creating and Sustaining Successful Growth, by Clayton M. Christensen and Michael E. Raynor, Harvard Business Review Press, 2013, p. 45.

[7] Henderson, Rebecca M., and Kim B. Clark. “Architectural Innovation: The Reconfiguration of Existing Product Technologies and the Failure of Established Firms.” Administrative Science Quarterly, vol. 35, no. 1, 1990, p. 9., doi:10.2307/2393549.

[8] “Chapter 3.” The Disruption Dilemma, by Joshua Gans, MIT Press, 2016.

[9] For an accessible discussion of the issues see: Kidder, David, and John Geraci. “CEOs Should Think Like Founders, Not Just Managers.” Harvard Business Review, 13 Nov. 2017, hbr.org/2017/11/ceos-should-think-like-founders-not-just-managers. Accessed 25 Oct. 2018.

[10] The Case for E-Commerce Acceleration (Aka, Bye Bye BBY?), by Jeff Jordan, a16z.com/2012/06/29/the-case-for-e-commerce-acceleration-aka-bye-bye-bby/. Adapted. Accessed October 21, 2018.

[11] Boricha, Mehul. “A Brief History of Video Technology [Infographic].” Tech Arrival, 12 May 2018, www.techrrival.com/video-technology-history-infographic/. Accessed 21 October 2018.

[12] Wedding, Nicole. “How Tech Disrupted The Music Industry: A Timeline.” Hybrid World Adelaide, 20 Sept. 2018, hybridworldadelaide.org/2018/03/27/tech-disrupted-music-industry-timeline/. Accessed 21 October 2018.

[13] In this case, generally, the music companies extract profits from the streaming platforms because there are fewer music companies than music streaming platforms. See Porter, Michael E. “The Five Competitive Forces That Shape Strategy.” Harvard Business Review, January 2008.

[14] Meyers, Justin. “From Backpack Transceiver to Smartphone: A Visual History of the Mobile Phone.” Gadget Hacks, Gadget Hacks, 5 May 2011, smartphones.gadgethacks.com/news/from-backpack-transceiver-smartphone-visual-history-mobile-phone-0127134/#ixzz1La40vQTO.

[15] Samsung, Huawei, Xiaomi, and OPPO all ship smartphones using Google’s Android OS.

[16] “Timeline of Photography Technology.” Wikipedia, Wikimedia Foundation, 4 Sept. 2018, en.wikipedia.org/wiki/Timeline_of_photography_technology. Accessed 22 October 2018.

[17] Analog photography relies on a chemical or electronic recording medium, with photographs ultimately printed on paper through chemical processing. In digital photography, arrays of electronic photodetectors capture and store images which are then processed as digital files only. Computational photography refers to the application of algorithmic processing to digital photography.

[18] Shih, Willy. “The Real Lessons From Kodak’s Decline.” MIT Sloan Management Review, 20 May 2016, sloanreview.mit.edu/article/the-real-lessons-from-kodaks-decline/?use_credit=a6ae29dde4b8fea84677452a90228c83. Accessed 22 October 2018.

[19] Kodak is trying to resurrect itself by focusing on new consumer demands and connecting with millennials — see Kodak + Forever21, InstantPrint Cameras, KodakOne and KodakCoin.

[20] Komori, Shigetaka. Innovating out of Crisis: How Fujifilm Survived (and Thrived) as Its Core Business Was Vanishing. Stone Bridge Press, 2015.

[21] Evans, Benedict. “The Scale of Tech Winners.” Benedict Evans, 13 Oct. 2017, www.ben-evans.com/benedictevans/2017/10/12/scale-wetxp.

[22] Amazon Alexa, Google Dot, Apple HomePod, for example.

[23] Gans, Joshua. “The Disruption Dilemma”, MIT Press, 2016. Page 40.

[24] This list is by no means exhaustive.

[25] Such a platform would make it relatively easy for a team of engineers to establish competing fashion companies using modular technology-enabled components which replicate everything large fashion incumbents do well, while simultaneously doing something that is valued by customers but which current incumbents cannot replicate without significant effort.

[26] Comment sent by Steve Hochman, via LinkedIn Messaging to Lisa Morales-Hellebo, on 15 October 2018.

[27] Ellen MacArthur Foundation, A new textiles economy: Redesigning fashion’s future, (2017, http://www.ellenmacarthurfoundation.org/publications). Accessed 23 October 2018.