About the Author

Mr. Aoaeh is a Cofounder and General Partner of REFASHIOND Ventures, an emerging venture capital fund manager that invests in early stage supply chain technology (#SupplyChainTech). He co-founded The New York Supply Chain Meetup and The Worldwide Supply Chain Federation. He is an Adjunct Professor of Supply Chain & Operations Management in the Department of Technology Management & Innovation at the Tandon School of Engineering at New York University. He is a VC-in-Residence at Genius Guild Greenhouse Fund, and a Venture Partner at Newark Venture Partners. From 2008 – 2018 he built the direct investing team at a single family office (2008 – 2011), and then built a standalone institutional early-stage venture capital firm based in New York City (2011 – 2018). He has been a charter holding member of the CFA Institute since 2017.

About REFASHIOND Ventures

REFASHIOND Ventures is a Supply Chain Technology (#SupplyChainTech) venture capital fund that invests in early stage innovations that refashion global supply chains. The fund sources deals from The Worldwide Supply Chain Federation’s global membership, and the general partners’ wide network of professional relationships in technology, supply chain, operations, venture capital, media, professional services, academia, and the public sector while leveraging their operating experience, and strong connections with corporations around the world as both potential investors and market-validating customers for REFASHIOND Ventures’ portfolio companies. REFASHIOND Ventures manages REFASHIOND Ventures Seed Fund, LP (REFASHIOND Seed) – a rolling fund on AngelList that is open to new investments from accredited individual investors, family offices and other types of investors.

Summary

Many more single- and multi-family offices are shifting capital to the venture capital asset class and away from other asset classes. In some instances such family offices are also seeking to do more direct technology venture capital investing. This is often motivated and driven by the desire of a younger generation of family members to direct capital towards innovations that will have a meaningful and positive impact in the world. It is worth examining some of the pitfalls that such an initiative can encounter with the aim of reducing the number of preventable mistakes that the people starting and managing such initiatives might make. I suggest a partnership model based on co-opetition and positive-sum partnerships rather than zero-sum rivalries between limited partners (LPs) – the family office principals and executives who wish to invest in venture capital through fund investments as well as direct investments in startups AND general partners (GPs) – the individuals launching and managing emerging venture firms to invest on the basis of novel and unique investment theses and strategies that account for the unique period of human in history in which we find ourselves. In this article early-stage investments refers to investments in Pre-Seed, Seed, and Series A startups. This report is uniquely deeply researched and is meant for senior decision makers at family offices in any part of the world seeking some help as they try to make sense of large volumes of sometimes contradictory and confusing information that is difficult to synthesize and distill into actionable conclusions.

- Author’s Note #1: This is not investment advice. Nothing in this article should be construed as legal advice.

- Author’s Note #2: The opinions expressed in this article are mine alone, except where I have included the ideas of individuals who contributed to the article. Any errors or omissions are my responsibility alone.

- Author’s Note #3: I hope that this article serves as a catalyst for further conversations; There is plenty of room for improvement, and I’d love to collaborate on expanding this work. It is already quite long, and I had to cut off some discussion to avoid making it even longer. If you want to discuss any aspect of this article, you can reach me by email at brian@refashiond.com. You can also reach me on Twitter, and LinkedIn. I would love suggestions about other material I should read on this topic and would be happy to discuss any section of the article in more depth with anyone who finds this topic as interesting as I do. (Wordcount: 25,036)

- Note: Originally published at refashiond.com on Friday, Dec 17, 2021.

Table of Contents

- Introduction

- A Summary of My Qualifications for Contributing to This Discussion

- A Brief History of Family Offices – What is the objective of a family office?

- A Brief History of Venture Capital – What is the main responsibility of an early-stage technology venture capitalist?

- The 3 Critical Challenges Faced By Most Emerging Venture Fund Managers

- The 3 Reasons That Make it Most Likely That A Family Office Will Fail at Tech Venture Capital

- Why Should Family Offices and Emerging Venture Capital Firms Partner?

- How Should Family Offices and Emerging Venture Firms Partner? (Half-a-Dozen Plus Three Ways)

- Market Voices: Fund Managers and other Practitioners Suggest How Family Offices and Emerging Venture Capital Firms Can Partner

- Family Offices & Emerging Fund Managers in Venture Capital: Playing The Right Game

- Conclusion

Introduction

These are exciting times in venture capital.

On November 23, 2021, the Financial Times ran Family offices become serious rivals to VC firms for funding start-ups by Stephen Foley. In the article he states that; “From wealthy individuals and family offices at the seed and early stages, to traditional asset and wealth managers getting in on pre-initial public offering rounds — not to mention hedge funds — investors that may have previously confined themselves to public markets are now clomping all over the VC landscape. Endowments and pension funds, the main providers of cash to VC funds, are also keen to cut out the middleman and invest in start-ups directly.”

I encourage the reader who is a family office principal or executive, or an investor at one of the other types of investment organizations that Foley says would traditionally have shied away from the private markets to read the rest of that article because it highlights some of the changing dynamics taking place in venture capital, shifts that are driving recent moves at firms like Sequoia, General Catalyst, Andreessen Horowitz, and others. Specifically, Foley points out that those moves are not “ . . . an illogical response to the deluge of capital chasing start-up investments, which suggests VC returns are likely to be lower than they were historically, even if they remain high relative to public markets.”

Towards the end of this article, the reader will get to hear directly from a number of investors who were kind enough to contribute to this article. Of note, Winter Mead, who runs a premiere community supporting emerging managers, partnered with First Republic Bank in 2021 to survey family office investment interest in emerging managers. The results of the survey demonstrated some interesting findings that support the increased interest in this category, including that 20% of family offices invest exclusively in emerging managers, and that 75% of family offices will invest in a first-time fund. There’s clearly interest in family offices and emerging managers understanding how to collaborate.

The purpose of this article is to help my fellow emerging managers better understand and productively collaborate with family offices, AND also to help family offices that are unsure how to engage with the dynamic and growing community of emerging venture capital fund managers better understand how they might engage more fruitfully with new venture firms pursuing unique and differentiated investment theses.

The discussion that follows applies only for early-stage technology investments, broadly speaking. Also, I am mostly thinking about emerging venture fund managers raising their very first institutional fund with family offices and relatively small institutional investors as potential limited partners.

A Summary of My Qualifications for Contributing to This Discussion

The portion of my professional experience that has direct relevance to this discussion starts in 2008. I spent the time between 2008 and 2018 at entities associated with Jeffrey Citron and his family’s family office – KEC Holdings, and KEC Ventures. That experience included: Managing two operational turnarounds simultaneously till mid-2012 – a fine-dining restaurant with locations throughout the United States, and a private jet charter company, together the 2 companies employed about 650 people and generated about $50 Million of top-line revenues; Representing the family office in negotiations with venture funds, private equity funds, hedge funds, and real estate funds in which the family office sought to make an investment as a limited partner; Assisting the family office’s CFO/COO with managing the family’s fund-of-funds portfolio between 2008 and 2012; Analyzing and making recommendations for public and private markets investments; Researching ideas that the family office considered incubating and launching – one of which was a brand new investment product for which we sought IP protection and pitched to potential outside investors and other partners; From 2011, I was entirely focused on building a standalone institutional early-stage technology venture capital fund that started from the initial fulltime team of 2 people, but that had grown to a team of 9 people in our HQ located in Midtown Manhattan by 2018 when I left to start laying the groundwork for REFASHIOND Ventures.

The topic of this article is one I have been thinking about since I started the interview process that led to the decade I spent at KEC Holdings from 2008 to 2011, and then at KEC Ventures from 2011 to 2018. It is a question I have continued to think about since 2018; How does one increase value for all the stakeholders of a mature company? How does one increase value for all the stakeholders of an early-stage technology startup? In this case; How can family offices and emerging venture capital firm managers collaborate as partners, and sometimes as friendly-rivals, in the dynamic and rapidly growing global market for technological innovation? What are some of the parameters on which such a partnership should be based?

Everyone who reads this article is benefiting from the experience and insights I have developed since 2008.

A Brief History of Family Offices – What is the Objective of a Family Office?

In The Family Office: A Comprehensive Guide for Advisers, Practitioners, and Students (Columbia University Press, August 2021), William I. Woodson and Edward V. Marshall observe that; “Family offices have been around in some form or other since civilization began in order to provide a vehicle for wealthy families to manage and safeguard their assets”. They further state; “The nineteenth century brought a surge in economic growth, industrialization, and wealth creation that far surpassed anything in history. Business empires sprang up and grew to enormous size. Family fortunes, as well as the need for family offices, expanded accordingly. Also encouraging the formation of family offices were the increased use of tax and estate-planning vehicles and the role of separate management companies.”

In describing the qualities of the people employed by family offices, Woodson and Marshall state that; “These families came to understand the key qualities needed of those who would serve them by running their family offices. Those qualities were—and remain today—loyalty, discretion, attention to detail, timely execution, business acumen, and faithful stewardship.”

Finally, Woodson and Marshall answer the question “What is a family office?” by stating that; “Family offices are entities set up by a single family, or by or for a group of families, to manage their assets and affairs. They are used to address the issues that come with substantial wealth, including dealing with complexity and helping family members achieve their goals (e.g., simplicity, purpose, legacy, family harmony, passing down wealth, investment management, philanthropy, and so on). In this context, family members are called “principals,” and the senior staff of a family office are referred to as “family office executives.” Principals are the primary members of the family that the family office supports, although there are situations where multiple generations and/or extended family members can use the services of a family office. Family offices vary in design, operations, and services delivered, depending on the needs of the principals.”

In my opinion, the most important task of any family office executive is wealth preservation, all other goals and duties are a distant second to wealth preservation. We will come back to this later. Woodson and Marshall outline 9 distinct types of family offices which can be grouped into 4 distinct classes.

In his book, The Family Office Book: Investing Capital for the Ultra-Affluent (Wiley Finance, 2012), Richard Wilson states; “Single family offices have existed in different forms for thousands of years. In the article “Family Offices in Europe and the United States” by Dr. Steen Ehlern, the managing director of the Ferguson Partners Family Office, noted that the merchants of ancient Japan and the Shang dynasty in China (1600 B.C.) both used multigenerational wealth management strategies. There are also several accounts of “trusts” being set up for the first time during the Crusades (A.D. 1100). Later, many wealthy banking families of Europe, including the Medicis, Bardis and Rothschilds, were said to have used a family office–like structure. These organizations often offered their services to other wealthy families, and in the late 1800s and 1900s they started to look more like modern day multi-family office operations. These operations grew out of single family offices that were asked to serve connected business families and out of private banks and early trust company establishments that were looking to serve more affluent clientele.”

According to Wilson;

- “Almost everyone who runs a single family office has between $100 million and $1 billion in assets, with a smaller percentage having over $1 billion and an even smaller percentage having under $100 million under management.”

- “Most multi-family offices require $20 million to $30 million in investable assets to join their platform, but due to economic conditions and hunger for business growth, some family offices are allowing $5 million and $10 million clients in the door.”

- “At the other end of the spectrum, some high-end family offices, including several we interviewed for this book, require $100 million to $250 million in investable assets to participate in their multi-family office.”

- “Due to technology and the ability to leverage taxation and risk management experts and consultants, I have found some successful single family offices with “only” $30 million to $50 million in assets.”

It should be obvious to the reader that family offices come in various flavors and sizes. One thing is constant, however; The family office’s first and primary objective is the preservation of its principals’ wealth and the smooth transfer of that wealth from one generation to the next without attracting too much attention from outside observers. However, the secretive world of family offices is undergoing some change. The secondary objective of every family office, and the various private foundations and endowments that they have created, is to grow the assets that the family, foundation, or endowment can draw upon in the future to support its activities.

That observation is supported by this December 2, 2021 article published by AsianInvestor, Succession planning, low yields among Asian family offices’ top concerns in which Natalie Koh explains that “Families are also haunted by fears that wealth does not pass three generations – a saying in different languages all over the world, and one that has been found to be largely true. Seventy percent of wealthy families lose their wealth by the second generation, and 90% by the third, according to a report by the Williams Group wealth consultancy.”

On November 11, 2021, writing for the Dallas Morning News in Family offices for ultra-wealthy with $100 million or more explode in Dallas and the U.S., Natalie Walters says “Recent data shows there are between 3,500 and 5,000 family offices in the world with one or more employees, $100 million or more in investible assets and some type of outside investment activity, according to a report from FINTRX, a family office research platform. Of those, 66% are in North America and 42% manage more than $1 billion in assets.” Walters adds that in the United States, “Texas is the state with the third-highest number of family offices, behind New York and California. Among cities, Dallas ranks third behind New York and Chicago.”

Walters quotes “Tayyab Mohamed of Agreus Group, a London-based recruitment company that works with family offices worldwide” who asserts that the financial crisis of 2008 caused a loss of trust, prompting many wealthy families to make the decision that they needed to take control of managing their wealth. As I pointed out in the brief summary of my professional experience at the beginning of this article, 2008 is also the year during which I started my tenure as a family office executive.

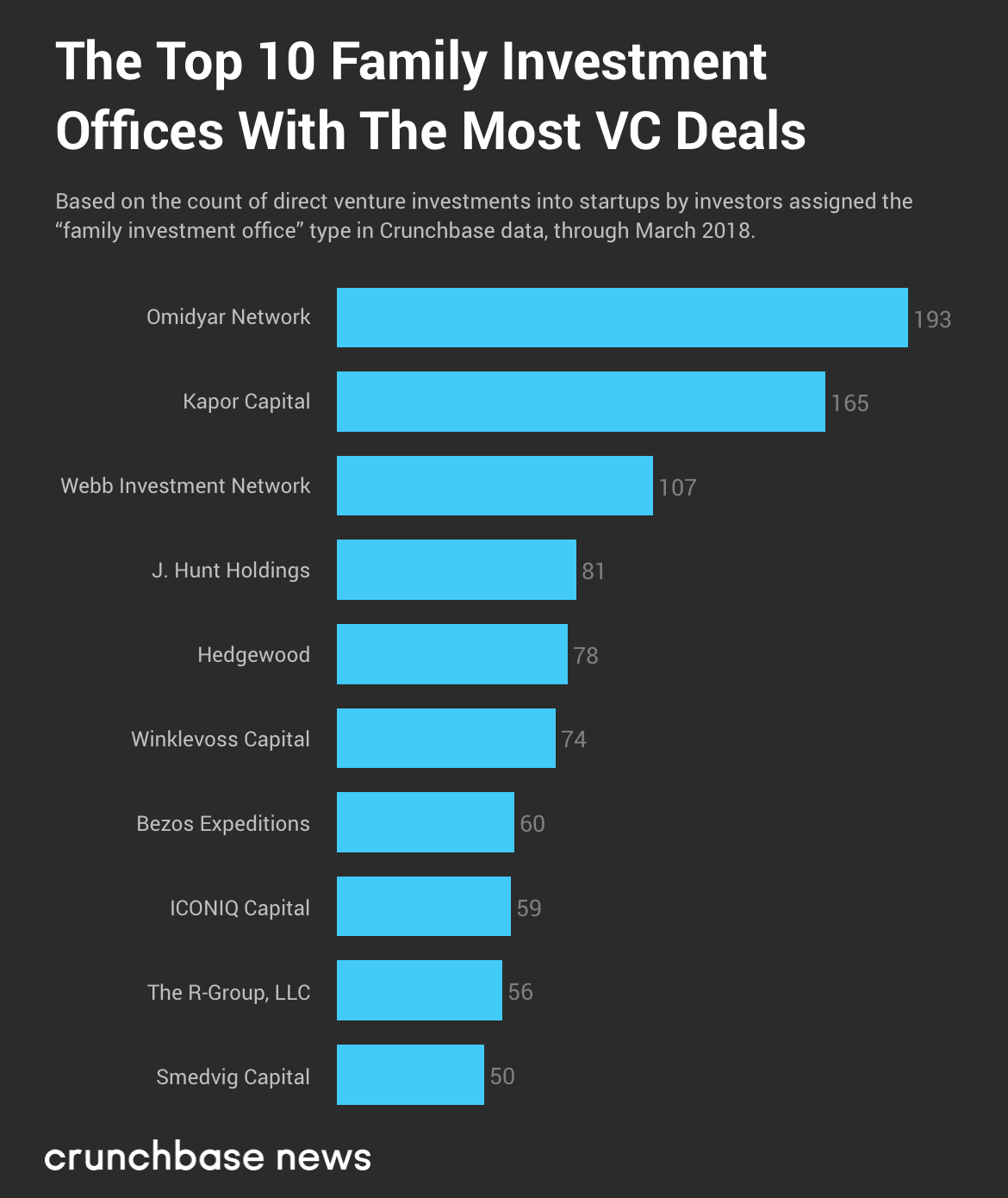

Writing for Crunchbase News on April 13, 2018, in The Top Ten Family Offices With The Most Direct Startup Investments, Jason Rowley states “There is some anecdotal evidence that more family offices are making their first investments directly into startups (as opposed to investing in a VC fund as a limited partner). But we wanted to know which investment groups have the most skin in the startup investing game, so to speak.” The following chart from that article summarizes the analysis.

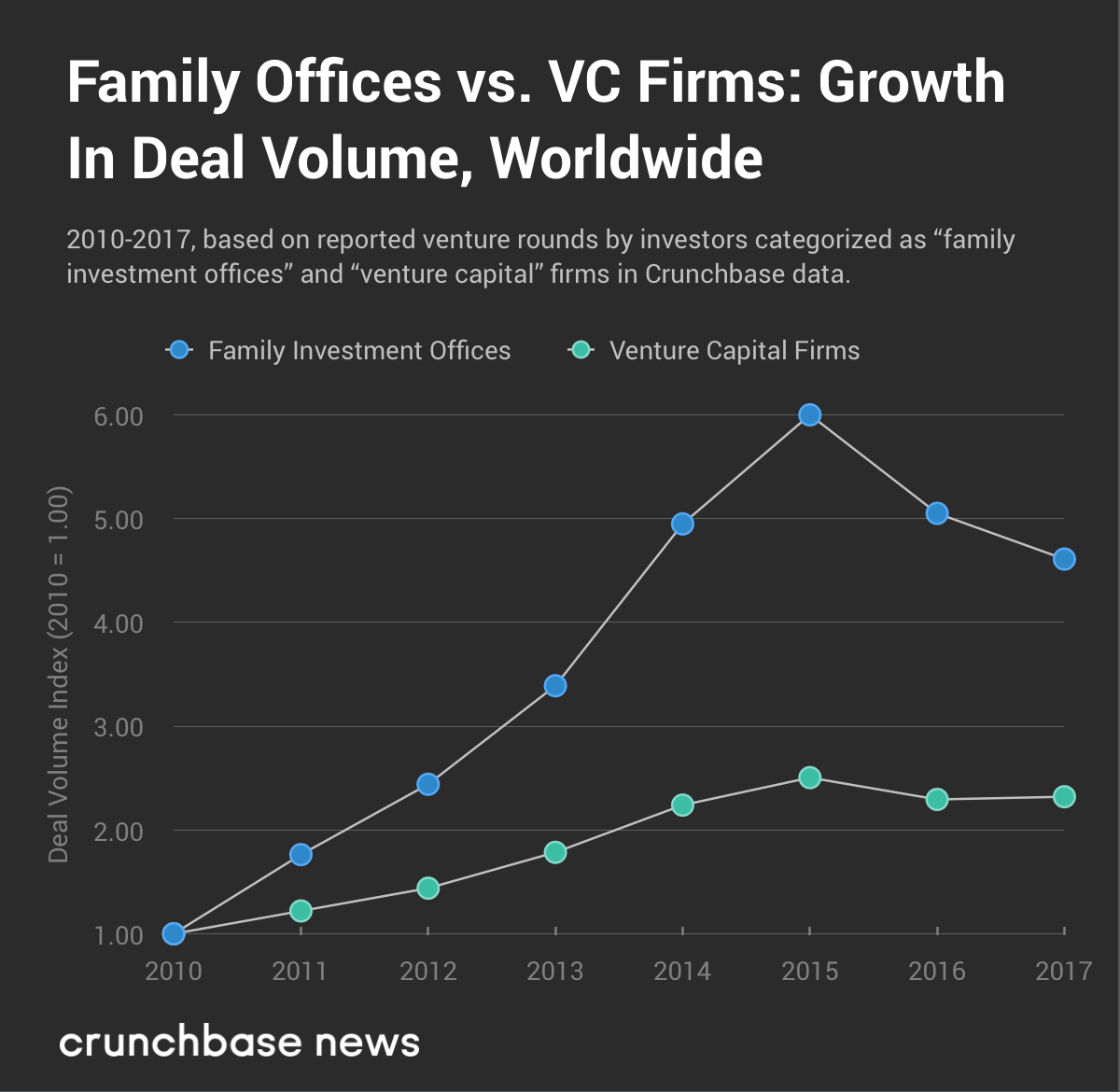

A few weeks before the analysis above, Rowley published Charting The Adoption Of Direct Startup Investments By Family Offices on March 26, 2018 in which he observed that “In relative terms, across a range of measures, deal volume growth was higher and faster among family offices than VC funds for a significant period of time. The data suggest that family offices making direct investments into startups recently became a trend. Especially for that period through 2014, family offices were on the early side of the adoption curve for making direct startup investments. Whatever growth we see on the VC side is the product of growth in the market in general, but it’s not like VC funds are still adopting direct startup investments into their repertoire. It’s been their model for decades. For comparatively stodgy family offices, it was still the new, new thing.” The graph below summarizes that statement.

Rowley makes another interesting observation in the article. He states that, “During the several years leading up to 2015, there was a run-up in the number of deals being struck. After that high point, though, deal volume began to decline in the US, which Crunchbase News has documented, as investors eschewed writing many smaller checks to early-stage startups and instead favored fewer, larger checks with later-stage tech companies. On a global scale, projected deal volume is roughly flat on an annualized basis from 2015 through 2017, whereas reported deal data is down primarily due to reporting delays. Since there are more U.S. family offices that invest in startups than international ones, it’s not surprising to see that family office deal volume hews closer to the U.S. market in general.”

We will come back to this point later.

An underlying factor that may be contributing to the phenomenon Rowley has reported on is that of the vast amount of wealth that has been created since the dot-com bubble by technology startups and companies located in Silicon Valley and other parts of the United States and the world. As the author of 7 Family Offices Behind Silicon Valley’s Tech Billionaires, published by Trusted Insight in November 2016, states “By any measure Silicon Valley has exerted an outsized influence on the tech industry and the world as we know it. Today the valley hosts nearly 40 companies on the Fortune 1000 list, a hundred private ‘unicorn’ companies valued at more than $1 billion and thousands of fledgling startups striving to be the next company to change the world.” The author goes on to say that, “This concentration of corporate success has created a vast network of high net worth founders and executives. In fact, 41 of the richest Americans on the Forbes 400 reside in Silicon Valley, and given the positive outlook on the 2017 IPO market, that number will surely grow.”

The trend highlighted by Trusted Insight has only accelerated since 2016, as a result the phenomenon Rowley reported on for Crunchbase News is likely to have accelerated as well. Although, I do not have data to support this assertion, I argue that globally, the number of family offices with business roots in, and potentially the amount of total wealth generated from, legacy industries outstrips that from Silicon Valley specifically, and technology more broadly irrespective of geographic location. Therefore, these trends will only accelerate as more family offices that did not originate from success in technology entrepreneurship undergo a generational transition with younger and more technology-savvy principals stepping into decision-making and leadership roles about how the family office invests its capital.

My former employer, UBS is arguably the world’s leading bank to family offices. In the 2021 edition of its UBS Global Family Office Report, the bank reports that;

- The majority of family offices it surveyed have investment priorities in; Health Tech (86%), Digital Transformation (82%), Automation and Robotics (75%), Smart Mobility (74%), and Green Tech (73%).

- Compared to 2020, in 2021 family offices are more likely to express a desire to become limited partners in private equity and venture capital funds, and more express an interest in making direct investments in startups and more mature companies; “There’s a sharp drop-off in the use of funds of funds, with investment in funds and direct investments rising significantly. 83% of survey respondents invest in PE. But while 37% of them invested in funds or funds of funds in 2020, that fell to 23% in 2021. Almost half (47%) invest in both funds and direct investments, up from 31% in 2020. Meanwhile, just under a third (30%) only invest in direct PE, a similar level to 2020. As a rule, direct PE is becoming more accessible, with secondary markets providing greater liquidity.”

- There’s growing interest in technological innovation and venture capital; “At a time when many young companies are growing fast, disrupting the incumbents, there’s a quest to invest in the innovators. More than three quarters (77%) of family offices make expansion/growth equity investments, with that proportion even higher in Switzerland (86%) and the US (92%).” The authors add, “Similarly, venture capital (VC) is the second most popular type of investment. Almost two thirds (61%) of family offices make VC investments; yet the proportion is higher still in Eastern Europe where three quarters (75%) do so.”

- Despite their growing interest in technological innovation and venture capital, family offices are more likely to fund expansion and growth stage investments in startups that have already been identified as technology innovators by upstream investors such as angel investors, and pre-seed or seed-stage venture funds: 79% of the family offices surveyed said they are not likely at all to make pre-seed investments; 57% are not likely at all to make seed-stage investments, while 35% are somewhat likely to make such investments; 26% are not likely at all to make early-stage investments, which I am interpreting to be Series A and Series B investments, while 46% are somewhat likely to make investments at this stage.

- Sustainable investing is a hot topic among family offices; “More than half (56%) of families invest sustainably, although with wide regional differences. Three quarters (72%) do so in Western Europe, a cheerleader for sustainability, while Eastern Europe lags at only a quarter (26%) and the US at 45%.” and “As the most dynamic asset owners, family offices appear to be leading the evolution to environmental, social and governance (ESG) integration, planning to increase allocations to about a quarter (24%) of the portfolios.”

- Impact investing remains a relatively small, but growing, part of family office portfolios; “Generally speaking, the number of impact investments is growing, notwithstanding the fact that it remains a relatively small part of portfolios. On average, family offices state they have impact projects across approximately six areas in 2021, versus four in 2020. While education still remains the most popular area, in 64% of portfolios, climate change matches it, up from 40% the previous year. Healthcare is also an area for 61%. Other increasingly popular areas include: economic development/ poverty alleviation, agriculture, alternative food sources and clean water and sanitation.” Moreover, “Different parts of the world have different priorities. In Western Europe, over half (52%) of family offices say that climate change has already influenced their investment choices. Meanwhile, Asia (43%) and the US (38%) say they have a pipeline of direct impact investment opportunities.”

- Lastly, about one-third of the family offices surveyed by UBS state that they are experiencing upward pressure on operating costs as they invest more resources to bolster their human capital and IT infrastructure: “More than a third (35%) report significant or moderate upwards pressure on salaries, while a further third do on IT (33%).”

It is worth reiterating the observation made earlier that; Every family office’s primary objective is the preservation of its principals’ wealth and the smooth transfer of that wealth from one generation to the next without attracting too much attention from outside observers. Obviously that does not take into consideration those family office principals who have chosen to distribute the vast majority of their wealth rather than pass it on as an inheritance to their heirs. Even then, in most such cases they are distributing that wealth to foundations and endowments, organizations that also function as institutional investors that disburse some of their assets to support the ongoing operations of their parent organizations while growing their capital base in order to fund their respective parent organizations’ missions and objectives in perpetuity, if possible.

A Brief History of Venture Capital – What is the Main Responsibility of an Early-stage Tech Venture Capitalist?

In his article, Venture Capital—Patronage to Apprenticeship to Profession (The Journal of Private Equity, Fall 2019), Joe Milam states; “Investing in creative or entrepreneurial ventures is part of the human condition and goes back as far as recorded history. The patronage of the Medici family of Florence supported the work of Leonardo de Vinci, Michelangelo, and Galileo. Queen Isabella was essentially a venture capitalist, supporting Christopher Columbus in his exploration of the New World. Many of the critical inflection points in modern history that had dramatic impacts on the human condition resulted from entrepreneurial initiatives supported by wealthy individuals and families. The history of modern venture capital was catalyzed by efforts at mobilizing capital for the many companies emerging after World War II, in part from both necessity and opportunity—the need to support the GIs returning from the war and the opportunity to commercialize the new technologies that resulted from the war effort. Commercial access and use of the Internet represents the latest catalyst for the acceleration in entrepreneurial activity around the world, with a corresponding growth in individuals investing in new ventures, as well as new funds.”

Some have argued that Queen Isabella of Castille should be recognized as the first venture capitalist, and the book Isabella of Castille (Bloomsbury, March 2017) by Giles Tremlett offers strong evidence for that argument. One wonders though, if there may have been other monarchs preceding Queen Isabella, in other parts of the world, who behaved in much the same way as Isabella did when she financed the voyage by Christopher Columbus. In no way am I attempting to diminish the import of what Isabella did, I am merely positing the possibility that this practice goes back even farther in human history than we may realize.

Two books, Creative Capital: Georges Doriot and the Birth of Venture Capital (Harvard Business Review Press, March 2008) by Spencer Ante and The First Venture Capitalist: Georges Doriot on Leadership, Capital, and Business Organization (Bayeux Arts, 2004) by Udayan Gupta paint the portrait of the man widely considered to be the father of Modern Venture Capitalism based on his role in conceptualizing, launching, and managing American Research & Development Corporation (ARD) in 1946.

What we can learn from Ante and Gupta is supplemented by David H. Hsu and Martin Kenney in Organizing Venture Capital: The Rise and Demise of American Research & Development Corporation, 1946-1973 in which they state that; “In contrast to venture capital firms formed contemporaneously by wealthy families such as the Rockefellers, Whitneys, and Payson and Trask, ARD was the only non-family venture capital firm— meaning it had to raise capital from other sources. ARD was also an experiment to see if a new organizational form created by the private sector could profitably discharge the function of funding the Schumpeterian process of creative destruction. It was an experiment that had four goals: (1) to nurture new firms and assist existing firms in upgrading their technology or adding new product lines, (2) to encourage the commercialization of technological innovations, (3) to contribute to an economic revival in New England, and (4) to assist in the diffusion of privately funded venture capital as an institution.”

The contemporaneous venture capital firms that were formed by wealthy families would be considered single-LP venture funds. Today single-LP funds typically have a wealthy family or a large corporation as the single limited partner.

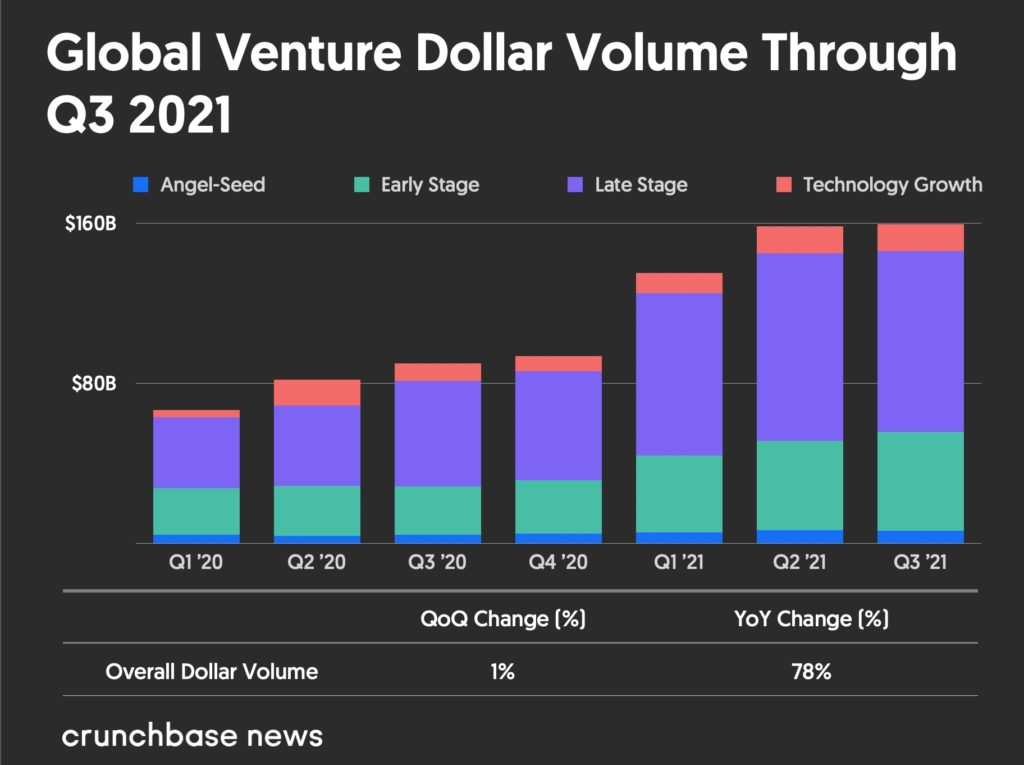

The venture capital landscape of today has certainly changed significantly since the days of ARD and its contemporaries. In The Q3 2021 Global Venture Capital Report: Record Funding Trend Held Strong which was published by Crunchbase News on October 26, 2021, Gené Teare observes that “Prior to 2021, global funding had not reached over $100 billion in a single quarter. Funding in 2021 has far superseded that amount, with the first quarter tracking at $135 billion, the second quarter reaching $159 billion, and the most recent quarter peaking at $160 billion.”

CBInsight’s State Of Venture Q3’21 Research Report which was published on October 7, 2021 adds some more color and context to the data from Crunchbase. Among other things, CBInsights reports that;

- “US companies raised $72.3B in Q3’21, making up 46% of global dollars — the most of any region. Funding grew 90% YoY, while also topping last quarter’s $70.3B.” The 3,210 deals that this represents was also a quarterly record.

- “Asia funding dollars rose 95% YoY to reach a record of $50.2B. Asia’s share of global equity funding rose from 26% in Q2’21 to 32% in Q3’21 — the only major region to see share growth QoQ.” In Asia, “China funding grew 26% QoQ to reach $25.5B. India funding jumped 68% QoQ and an astounding 195% YoY to $9.9B.”

- The world is birthing more unicorns at a faster and faster rate; “Q3’21 saw the global unicorn herd reach 848. This is 311 more than this time last year. In Q3’21, 127 new unicorns were born — the 2nd highest birth rate ever after Q2’21’s 140.” And; “Half of the new unicorns came from the US, with 69. Asia saw 30 and Europe 15.”

One more source of data to help us put things in context is These 6 charts show how much VC is awash in capital in 2021 published by Pitchbook on October 17, 2021. In that article, Alexander Davis states, “More often than not in today’s market, funding rounds involve asset managers, hedge funds, corporate venture and other so-called nontraditional investors invading the VC market. And companies raising those funding rounds are increasingly commanding much higher valuations, at least in part because nontraditional investors are typically less price-sensitive than their peers in the VC mainstream.”

In other words, family offices investing in the venture capital asset class are competing with venture capital firms, as well as with a more varied array of well resourced organizations each seeking the same growth and expansion stage opportunities that UBS has already told us family offices seek.

Davis adds, “Look for more of the era of high price multiples to continue as nontraditional investors bulk up. Often tagged as venture market “tourists,” this group together is sitting on $350 billion worth of investable capital, according to PitchBook estimates.”

This begs the question; What precisely is the primary responsibility of an early-stage venture capitalist? I propose that the singular responsibility of every early-stage venture capitalist is to harness extreme uncertainty AND informed, educated guesses about what we can not yet know about the future to generate outsized financial returns for the benefit of the limited partners that have invested in the venture capitalist’s fund. Assuming the reader accepts that proposition, this immediately leads to another question; How does the early-stage venture capitalist harness extreme uncertainty AND informed, educated guesses about what we can not yet know about the future to generate outsized financial returns?

Richard Zeckhauser, the Frank P. Ramsey Professor of Political Economy, at the Kennedy School, Harvard University offers a useful framework for thinking about how early-stage venture capital investors fulfill their responsibilities to their limited partners in his paper, Investing in the Unknown and Unknowable (Capitalism and Society, Vol. 1, Issue 2, Article 5, 2006). While the entire paper is worth reading, here are some observations that stand out to me;

- Unknowable situations are widespread and inevitable; Will COVID19 continue to get worse, or will it be tamed so that the world can return to a state resembling what existed before the pandemic? What will the near term impact of the Climate Crisis be on global trade and livelihoods? Are the current disruptions affecting global supply chains a temporary phenomenon, or are they merely symptoms of a more permissive underlying problem? Will geo-political tensions continue to escalate, and what does this mean for global trade and commerce? I am not certain that these are even the right questions one should be asking given the current state of affairs in the world, but they offer as good a starting point as any, in my opinion.

- Most investors avoid the unknown and the unknowable because we are mostly trained to gravitate towards certainty, where we assume that we know the states of the world and can assess and assign probabilities.

- Unknown and unknowable situations have been, and will continue to be, “associated with remarkably powerful investment returns.”

- “There are systematic ways to think about unknowable situations. If these ways are followed, they can provide a path to extraordinary expected investment returns. To be sure, some substantial losses are inevitable, and some will be blameworthy after the fact. But the net expected results, even after allowing for risk aversion, will be strongly positive.”

- To avoid speculators, investors might consider investing in situations that are unknown, unknowable, and unique (UUU) because this creates an opportunity for the investor to get in at an attractive low price.

- Success at investing in UUU situations requires that the investor has devoted some time and effort to understanding and identifying the “general characteristics of when such investments are desirable, and when not.”

- In the UUU environment, investors with complementary skills exhibit a “combination of scarce skills and wise selection of companies for investment” and they gain difficult to duplicate access to investment opportunities because of the complementary skills that they have honed over time. Furthermore “Individuals with complementary skills enjoy great positive excess returns from UU investments. Make a sidecar investment alongside them when given the opportunity” because most investors “could never learn about the unknowables sufficiently well to do traditional due diligence.”

- “The major fortunes in finance, I would speculate, have been made by people who are effective in dealing with the unknown and unknowable. This will probably be truer still in the future. Given the influx of educated professionals into finance, those who make their living speculating and trading in traditional markets are increasingly up against others who are tremendously bright and tremendously well-informed.” Reiterating an observation I have made previously in this article; One has to wonder how well the 79% of family offices whose response to the UBS Global Family Office indicates a preference for later stage investments will fare against the influx of capital from the clamoring horde of other nontraditional investors chasing alpha.

In sum: First; Early-stage venture capitalists generate returns for their limited partners by investing in the Schumpeterian process of creative destruction; Second; This is a process characterized by extreme uncertainty, with unique investment opportunities that benefit from future outcomes and states of the world that are unknown, and unknowable. Those venture capital firms that succeed in this endeavor do so by investing significant time and effort to develop skills, knowledge, collective and individual reputations, and social networks that are complementary to their investments – meaning that they have a unique ability to employ information asymmetries and a lack of competition to their advantage in the ways that are most relevant for the conversion of unrealized investment returns into cash distributions to their limited partners. Third; the best returns are to be found by investing where one is not consistently competing against many others who are “tremendously bright and tremendously well-informed.”

The 3 Critical Challenges Faced By Most Emerging Venture Fund Managers

Launching and building a brand new venture capital firm is no different from building a new startup. New venture firms face the same challenges that young startups face. Here are 3 challenges that can prove fatal to any new venture firm setting out to raise its very first fund.

First; Failing to raise a sufficient pool of capital with which to effectively implement, execute, and test the investment thesis. Emerging managers who are raising their very first fund are particularly susceptible to this problem because there is a pervasive belief amongst limited partners that the only venture funds worth investing in are funds in the top 5% measured by historical performance.

Assuming one ignores the common disclaimer in finance and investments that “Past performance is no guarantee of future results,” the evidence suggests that limited partners would do well to cast a wider net. Has Persistence Persisted In Private Equity? Evidence From Buyout And Venture Capital Funds is a November 2020 paper authored by Robert S. Harris, Tim Jenkinson, Steven N. Kaplan, and Ruediger Stucke in which they find that; Among VC funds “. . . for the overall sample, first-time funds have an average PME of 1.24 close to the average for previous funds in the 2nd quartile. Post-2000, first-time funds do even better with an average PME of 1.23 that exceeds (albeit not significantly) the average PME of those with previous top quartile funds.” PME stands for Public Market Equivalent and is a measure the authors use to compare the performance of the buyout and VC funds in their study with the S&P 500. Their conclusion calls into question limited partners aversion to first-time funds, assuming the goal is to beat the S&P 500. It is fair for limited partners to ask how first-time fund managers perform in comparison to the NASDAQ.

Second; Winning deals when there’s a large number of firms pursuing a similar or identical investment thesis, and adverse selection. For a fund manager raising a first fund, winning deals can be a tall task for a number of reasons: First, if the manager’s investment thesis isn’t sufficiently differentiated, the phenomenon Zeckhauser described comes into play. That is, the manager enters into competition with potentially better resourced peers who can offer startup founders the potential for follow-on capital if the startup goes on to raise subsequent rounds of financing, for example. If the manager lacks brand-recognition or has not yet earned a reputation that causes startup founders to proactively want to work with that manager, then, in an environment such as exists now, the new manager is mainly offering a commodity.

Adverse selection is closely related to new managers’ ability to win deals. Adverse selection can be thought of in the words of Jay Z, rapping in his song Numb/Encore with Linkin Park, in which he says “when you first come in the game, they try to play you.” Again, in situations where the first-time fund manager is not pursuing a sufficiently differentiated investment thesis, there’s a tendency for already established venture fund managers and angel investors to flood the new manager with “warm introductions” to startups the established managers and angel investors have already invested in that are struggling to raise capital. This is particularly true when the new manager is perceived to be an outsider to the venture capital and tech startup community – the situation I found myself in starting in 2011, and to a great extent still the situation I find myself in today.

The difference now is that, starting around 2015, I have invested an enormous amount of time, energy, and personal capital in: Developing a #SupplyChainTech thesis that is pretty unique and that forms the basis for the investments my co-founder and I make at REFASHIOND Ventures; Building an extensive and global social network; Bootstrapping the world’s first open and grass-roots driven community of practice for people who are obsessively enthusiastic about supply chains, innovation, and technology; Embracing the challenge of teaching a Supply Chain & Operations Management course at the Tandon School of Engineering at New York University; Embracing the challenge of writing a weekly column focused on the early-stage technology innovations with the potential to refashion global supply chains for the two years between April 2019 and April 2021 at FreightWaves, arguably the world’s most visited portal for news about freight technology.

You have every justification to ask; To what end? As Zeckhauser points out in his paper; “Similarly, the more difficult a field is to investigate, the greater will be the unknown and unknowables associated with it, and the greater the expected profits to those who deal sensibly with them. Unknowables can’t be transmuted into sensible guesses — but one can take one’s positions and array one’s claims so that unknowns and unknowables are mostly allies, not nemeses. And one can train to avoid one’s own behavioral decision tendencies, and to capitalize on those of others.”

When we get warm introductions to startups that fit our #SupplyChainTech thesis at REFASHIOND Ventures it is relatively easy for us to verify that we are not falling victim to adverse selection, either directly, based on our own knowledge, or through our extensive network. To minimize the risk of adverse selection, we encourage startup founders to eschew so-called warm introductions and to seek us out directly. We make exceptions in situations where the introduction would be coming from a potential co-investor in the same round of financing, or someone for whom there’s a thesis mismatch but who thinks the founder is so impressive and promising that they recommend we take a meeting.

Third; A failure to raise the second fund after having raised the first fund. This can happen for a number of different reasons; Operational failures. Poor investment decision-making leading to too many poor outcomes in the portfolio. Personnel issues that arise after the fact. Failure to cultivate the social network and other relationships necessary to propel and accelerate the performance of startups in which the fund has made an investment. Etc. However, for this discussion, the reason that concerns me most is that sometimes a first-time fund will fail to raise its second fund because it lacks a strong and sufficiently diverse limited partner base in its prior fund to enable it to raise the successor fund. For example, this could happen if the first fund is a single-LP vehicle, and it could happen for any number of reasons. This could also happen if an anchor limited partner that accounts for, say, 20% or more of the current fund becomes unable or unwilling to commit to the succeeding fund, and the general partner has not yet cultivated a relationship with another family office that can replace the limited partner that is being lost.

The 3 Reasons That Make it Likely That A Family Office Will Fail at Tech Venture Capital

Let us temporarily set aside family offices founded by individuals who have made their wealth by founding or being early employees at technology startups that have gone on to achieve a major exit. We may then view the remaining family offices that are considering a foray into direct or fund investments in venture capital to be outsiders.

We have already seen that interest from family offices in venture capital, and direct investments into startups is not a new phenomenon. Be that as it may, family offices’ justified focus on wealth preservation as their primary goal, with growing that wealth being the important secondary goal, leads to certain invisible traps that make it difficult for the average family office to execute an early-stage technology venture capital investment strategy successfully.

First; Many family offices newly making forays into direct venture capital investing tend to fall victim to Overconfidence Bias. This blindspot is exacerbated by the phenomenon of Adverse Selection that such outsiders to the startup and venture capital community encounter when they first start participating in the community as investors. But, that is not all, Overconfidence and Adverse Selection are amplified by an Illusion of Knowledge. Zeckhauser makes two observations relevant to this issue: First, “When individuals are assessing quantities about which they know very little, they are much too confident of their knowledge (Alpert and Raiffa, 1982);” Second, “Individuals who are overconfident of their knowledge will fall prey to poor investments in the UU world.” Where UU stands for Unknown & Unknowable. The illusion of knowledge can arise because family offices could be relying on knowledge about the state of the industry in which the family generated its wealth that is no longer relevant given more recent developments in that industry’s adoption and use of technology. Without understanding that a given startup is developing what might qualify as a supply side innovation, family office principals and executives might frequently dismiss investments that go on to perform phenomenally well, while investing too often in startups that fail.

Overconfidence, accentuated by an Illusion of Knowledge can result in family offices: Being concentrated in a relatively small number of startups – a number too small to maximize the potential to capture power law effects; Allocating too much cash into the first investment in each of the small number of startups in which the family office makes an initial investment; Not being diversified enough to maximize their odds of success given the high failure rates of early-stage technology startups; Overpaying for the startups in which they make an investment, thereby accentuating the problems I have outlined before this.

I do not mean to suggest that venture capitalists are somehow immune from Overconfidence and Illusion of Knowledge, since they are just as susceptible to those psychological biases as anyone making similar investment decisions at a family office. However, all else equal, there are aspects of venture capital practice that make it less likely that the average venture capitalist will succumb to Overconfidence and Illusion of Knowledge

Second; Family offices underestimate the amount of time, and mental, physical, and emotional energy it takes to build a successful early-stage venture capital investing practice. Most outside observers make the same mistake. The sheer volume of work required to succeed in early-stage venture capital makes it unlikely that the principals and executives of a given family office possess the predisposition, stamina, and enthusiasm for the punishing amounts of work that is required to build an early-stage technology venture practice that will match or beat even the worst independent venture capital firms in the performance brackets the family office desires most.

Third; Family office principals and executives who are new to venture capital investing generally do not understand the nuances of Power Law Distributions and Portfolio Construction. As such they fail to create internal processes and decision-making procedures that enable them to benefit from the Power Law phenomena that drive venture returns. (Author’s Note: The reader who is unfamiliar with Power Laws and the role they play in early-stage venture capital should read this and this. I have researched the issue of portfolio construction from practitioners’ perspectives quite exhaustively, including input from other VCs in a discussion on Twitter here and distilled in a blog post here NotesOnStrategy | Seed-stage Venture Capital Portfolio Construction.)

The problems encountered due to insufficient knowledge of Power Law phenomena and Portfolio Construction might arise because investments require consensus, but family office executives may defer to family office principals rather than offer their true personal opinions about specific investments the family office is pursuing; This is understandable since, for the family office executive, there’s no possible career upside to be gained from wrongly assessing uncertainty or engaging in emotionally fraught debates with family members.

Another way family offices may fall into this trap is that decisions about investments often, but not always, require the final approval of a family office principal who is insufficiently connected to the work that goes into assessing a specific startup investment. By their nature, the startups that generate outsized returns are highly non-consensus AND non-obvious at the early-stage of their lifecycle. As a result, family office principals are always making decisions based on incomplete and imperfect information, a situation that can be made significantly worse if the principals are not fully dialed-in, and fully engaged, with the due diligence and research that is a part of the investment decision-making process. The most likely outcome then is obvious; An anti-portfolio with too many winners AND a portfolio with too few winners.

Venture capitalists prefer to invest in startups that will benefit from network effects, and venture capital itself is a network effects AND hits driven business. This explains the behavior of many venture capitalists. Contrast this with the typical family office’s desire for privacy, discreetness, and discretion, staying away from the spotlight. Relatively speaking, this puts family offices at a great disadvantage to the venture capitalists with whom they ostensibly wish to compete. (Readers who are curious about Network Effects can access a discussion here.)

As a result family offices might source the startups in which they invest from a very narrow circle of financial advisors, investment bankers, lawyers, tax experts, and from their friends, close associates, and other acquaintances, while venture firms are constantly refining their deal sourcing strategies to ensure that they cast their nets as wide and as far as possible – adopting both push and pull strategies, and in some cases, developing proprietary software to enable deal-sourcing at scale, in addition to all the other less tech-enabled approaches they implement.

This April 17, 2015, article in the Jakarta Globe, Family Offices in Asia, the Middle East to Double, Insead Says, highlights this challenge. The author, Klaus Wille, points out that family office principals can interfere with investment decision-making in ways that are erratic and unpredictable making asset allocation problematic, as well as making it challenging for family offices to attract top investing talent. To be completely blunt about it, when it comes to deal sourcing, investment decision-making, and the ability to compete and get into the financing rounds of early-stage technology startups that independent venture capital investors consider attractive, most family offices are bringing a cute, itsy-bitsy plastic butter knife to a proverbial gunfight while venture capital firms are showing up with a range of vehicle mounted machine guns. Or, as Fred Destin, a prominent European venture capitalist put it in a discussion on LinkedIn that started with this post by Ronald Diamond, Founder & CEO of Diamond Wealth, about family offices competing with and disrupting traditional venture capitalists for startup investments, “Good fucking luck. It’s hard for us to get into deals with all the energy we throw at it, and it’s not like our terms are heavy.”

These are problems that can be solved if family offices are willing to consider alternatives to going it alone, and play the right game, when they first make a foray into early-stage technology venture investing. But before we discuss possible solutions, we must first examine why this period of human history particularly calls for such partnerships.

Why Family Offices and Emerging Venture Capital Firms Should Partner

In their January 2020 article, Venture Capital Positively Disrupts Intergenerational Investing, Maureen Austin and David Thurston, both managing directors at Cambridge Associates observe that “Families of wealth face three key questions about intergenerational wealth planning: how best to invest to sustain future generations; how best to engage the next generation; and how best to ensure family unity endures. Often each question is addressed independently.” In the rest of the paper Austin and Thurston point out that;

- “Venture capital investing offers exposure to evolving industries, often at the ground level, hedging the risks associated with mature companies ripe for disruption.” Furthermore, Austin and Thurston argue that the macro environment favors continued relative outperformance of the venture capital asset class when compared to public markets because “Technological advancements, strong entrepreneurial talent, availability of capital, and fund manager skill are creating intriguing investment opportunities across multiple dimensions.”

- Although no two families are the same, family office principals and executives should consider allocating 40% or more to private investments. Furthermore, they suggest that family offices should dedicate “half of their private investment allocations to VC, provided these families have a long time horizon and the requisite liquidity provisions to meet their spending needs. Factoring in the potential tax advantages of VC investing—such as returns being taxed primarily as long-term capital gain; opportunities to discount interests for gift, estate, and inheritance tax purposes; and possible qualified small business stock tax treatment—a 20% allocation can nicely position a portfolio for future generations.” This point is emphasized in Cambridge: Family Offices Can Outperform With More Private Investment, a February 2019 article published by Institutional Investor, in which Alicia McElhany states that, “According to Austin’s colleague, Andrea Auerbach, who leads the firm’s global private investments group, some family offices have been around for longer than endowments or foundations. “That longevity favors private investment strategies,” she said by phone, adding that tying up assets for at least ten to 15 years in private investments can improve performance.” In the same article, McElhany observes, “Cambridge arrived at a 40 percent allocation by analyzing the endowments and foundations in the top quartile of performance. The firm found that those in the top quartile had allocated at least 15 percent to private investments, while those in the top decile had steadily increased their private investment allocations over the past 20 years, coming close to or passing 40 percent.”

- “VC investors during the 2000 tech bubble experienced significantly varied results, with both big winners and big losers. Since then, the industry has evolved, and fund managers have learned valuable lessons that benefit today’s venture investors. What once was considered a bingo card approach to fund construction has been replaced with a more rigorous, risk-managed assembly of companies. VC funds are surrounding themselves with “incubator” forums and core communities of advisors, as well as setting aside capital for follow-on needs. These additional measures provide critical resources that enable start-up companies to find solid product market fit and to scale accordingly. This has had the dual effect of reducing return dispersion among managers and reducing the impairment and capital loss ratios of the underlying universe of companies.” They add, “Investing in venture funds, which each have 20–30 investments, reduces the risk from any single start-up. Diversifying across multiple funds helps to mitigate the downside probability of overall loss.”

The rest of the article by Austin and Thurston is worth reading. It contains data that puts the observations and suggestions they make into fuller and more complete context.

In their book, 21st Century Investing: Redirecting Financial Strategies To Drive Systems Change, William Burckart and Steve Lydenberg observe that “Many investors increasingly understand that the two objectives of making money and solving global challenges are not just compatible but synergistic.” They add that “Finance and investment are built on the predictability and reliability of society, the financial system, and the environment. These systems are important, really important. Stable systems promote healthy markets; unstable systems lead to reduced or negative market returns. And the decisions made daily by investors—institutions and individuals—impact the fate of these systems inevitably and powerfully whether these investors recognize that or not.”

According to Burkart and Lydenberg, System-Level Investing is investing that deliberately, intentionally, proactively, and methodically “set out to manage their impacts on the largest, most important global systems. They deliberately adopt investment strategies that seek to minimize systemic risks at these levels and promote opportunities for system-wide rewards.” While all investors affect global systems, true systems investors can be identified because they actively align themselves and their investments with society’s long term goals.

Coincidentally, there is a rising cohort of emerging managers that fit squarely within Burkart and Lydenberg’s Systems Investing framework.

For example: My friend and teammate, Kathryn Finney is Founder & CEO of Genius Guild and Founder & General Partner of the Genius Guild Greenhouse Fund. Genius Guild is a business creation platform that uses the venture studio model (Fund + Content + Community) to invest in high growth companies led by Black founders that serve Black communities and beyond. The company’s vision is to build and invest in market-based innovations that end racism. Similarly, my friend and teammate, Tessa Flippin is Founder and Managing Partner of Capitallize VC, a venture capital fund reducing racial wealth disparities through investments in Black and Latinx founders. (Author’s Note: Tessa and I serve as VCs-in-Residence at Genius Guild).

Given my past experience sourcing emerging seed-stage venture fund managers who, nearly a decade later, are now praised for benchmark beating performance, I believe that Finney and Flippin are both very uniquely positioned to execute on their respective investment theses, and with adequate capital would run circles around most family offices that decided to compete against them head-to-head. Moreover, they are each very advantageously positioned to compete and outperform other emerging fund managers pursuing similar investment theses: Finney was focused on the issues at the core of Genius Guild’s investment thesis before those issues became socially-acceptable and popular. She has gained insights, experience, and has built a network of relationships that would take more than a decade of experience for someone else to replicate; Flippin’s experience as an early-stage venture capital investor and startup founder with experience and roots that span the United States and Latin America informs Capitallize VC’s thesis, and that is not so easy to replicate either.

At REFASHIOND Ventures we believe that supply chains are a complex, global intersection of social, technological, economic, and environmental systems. If any of those subsystems fails, supply chains break down and fail too – as the COVID19 Pandemic has demonstrated all too clearly. Our investment thesis centers on early-stage technology innovations that refashion global supply chains to make them fit-for-purpose in the face of: The Climate Crisis and increasingly damaging severe weather events; Increasing geo-political tensions between the West, China, and Russia; Increasingly demanding consumers all over the world, and; Corporations that now realize that supply chains are the basis on which competitive advantage is won or lost, amid increasingly strident calls from consumers and regulators for industrial supply chains to stop and in some cases reverse the damage that man-made supply chains have caused the natural environment, causing corporate executives to seek investments in innovation and technology.

Taking things a step further, we argue that: Supply chain innovation is the basis on which all sustainable innovation occurs, AND; The goals that Sustainable, Impact, Climate, and ESG investors seek are only actualized through industrial supply chains.

Other Systems Investing areas that are attracting new fund managers, as well some established managers are: Climate Change; Diversity, Equity, and Inclusion; Impact Investing; Environmental, Social, and Governance (ESG) Investing; And Sustainable Investing.

Referring to social, financial, and environmental systems, Burkart and Lydenberg state, “Understanding these systems – and ensuring their resilience – is more important than ever. Because we live in an increasingly populated, complex, and interconnected world, a disruption in one can cause multiple others to fall like dominos in a line.”

Burkart and Lydenberg’s Systems Investing framework ties in directly with what appears to be a growing wave among family offices and their approach to how they conduct their affairs. In this March 25, 2021 article published by Forbes, Family Offices: Identifying And Incorporating Sustainability Into An Investment Strategy, the author, Mariett Ramm, who is also a family office associate who advises on investment strategies and plans states that “Generating returns financially is, of course, one of the main priorities when opting for any asset class, but I believe we cannot ignore ethical and environmental factors when it comes to responsible investing. Environmental and social considerations should no longer be viewed as negative externalities but rather exciting challenges that newer generations of family offices can embrace with open arms. It is all about making an impact.”

Buttressing Ramm’s observations, the November 4, 2021 article, Doing Well by Doing Good – The Impact of Family Offices, published by Tharawat Magazine features an interview of Tobias Prestel, Founding Partner and CEO at Prestel & Partner, Germany by the author, Tony Sekulic. Prestel makes the observation that “Today’s wealth owners are far younger; much of the world’s wealth has already been transferred from one generation to the next. Next-gens are holding the reins now, and they typically have a different mindset than their predecessors in the 1980s and 1990s. As such, they use their wealth differently.” Adding that, “The most significant trend right now is the move towards impact investing. More than any other that has come before, this generation is interested in what we call ‘doing well by doing good.’”

In a December 4, 2021 article published by Fast Company, Venture capital isn’t working for the 99%, the author, Michael Basch, who is a Managing Partner at Atento Capital in Tulsa, Oklahoma argues that venture capital can only truly fulfill its potential to transform society “if we all work together: Nonprofits and fund managers, local governments and investors, all coming together to give more Americans the chance to achieve their potential, making our nation richer not just in wealth but in opportunity for all.” That is similar to an argument I made in my January 22, 2021 column at FreightWaves, Commentary: Time to turn rest of US into innovation factory. The truth is that, more so than in the past, today a significant number of emerging managers are raising their firms’ very first funds and are pursuing investment theses to make venture capital work for the 99%, but they lack access to capital from limited partners.

Two recently published books offer different but complementary perspectives on why supply chain technology is going to be a significant pivot-point on which developments in the 21st Century will rest.

In Arriving Today: From Factory to Front Door — Why Everything Has Changed About How and What We Buy (HarperCollins, September 2021), Christopher Mims, a technology reporter and columnist at the Wall Street Journal explores how consumers’ behavior and expectations for instant gratification and convenience is stressing global manufacturing, logistics, and retail systems, networks, and platforms. This trend is not going to ease up. It is going to get worse. Coincidentally, Mims started and finished working on the book just as the COVID-19 pandemic broke. He gives readers a bird’s eye view of what the near future of global retail operations and value chains might resemble by following the journey of a USB stick from the factory that makes it in a town in Vietnam to the front door of the end consumer in suburban Greenwich, Connecticut just outside New York City.

In The Exponential Age How Accelerating Technology is Transforming Business, Politics and Society (Diversion Books, September 2021), Azeem Azhar argues that we are living in an age of technology that is accelerating beyond the ability of the average person to keep up or even understand the impact that important general purpose technologies will have on all aspects of human civilization – society, business, economics, politics, culture, technology itself, the environment, etc etc. As he states in The Exponential Age Will Transform Economics Forever, an article published in Wired UK on September 6, 2021, “for all the visibility of exponential change, most of the institutions that make up our society follow a linear trajectory. Codified laws and unspoken social norms; legacy companies and NGOs; political systems and intergovernmental bodies – all have only ever known how to adapt incrementally. Stability is an important force within institutions. In fact, it’s built into them. The gap between our institutions’ capacity to change and our new technologies’ accelerating speed is the defining consequence of our shift to the Exponential Age. On the one side, you have the new behaviours, relationships and structures that are enabled by exponentially improving technologies, and the products and services built from them. On the other, you have the norms that have evolved or been designed to suit the needs of earlier configurations of technology. The gap leads to extreme tension. In the Exponential Age this divergence is ongoing – and it is everywhere.”

In the context of the ongoing COVID-19 pandemic, what Mims and Azhar document is that our world is undergoing a transition in which how we make, store, move, and consume things is undergoing a fundamental transformation. In the context of the Climate Crisis and the challenges it poses for the future, their books raise profound questions about how industrial supply chains will adapt in a future that is more volatile, uncertain, complex, and uncertain.

According to the UBS 2021 Global Family Office Report, when family offices were asked why they are putting so much faith in Sustainable Investing, “The most popular answer is a sense of responsibility – it’s for the positive impact on society, according to almost two thirds (62%). Similarly, more than half (55%) say it’s the right thing to do for society. Roughly half (49%) also see it as being the main way to invest in [the] future.” In this specific instance, I am assuming that Sustainable Investing includes ESG and Impact Investing, and perhaps even Climate.

So far in this discussion, I have mainly had traditional family offices in mind: Traditional Family Offices may be Single Family Offices or Multi Family Offices. If they are Multi Family Offices, they may be private or commercial, some may be Virtual Family Offices. Some may focus exclusively on direct investments, meaning that they focus their investing almost entirely in the private markets. Another type of family office that could benefit from investing in the venture capital asset class and partnering with emerging managers, particularly those raising their first fund, if it is not doing so already, is the Embedded Family Office.

An Embedded Family Office does not stand alone as an independent entity but instead is integrated tightly into a privately or closely held family business. The family business could be a conglomerate or could pursue a single line of business. According to Woodson and Marshall, Embedded Family Offices resemble Single Family Offices in the activities and investments they pursue, and are mainly grouped in a category unto themselves “largely because of their association with a closely held family business.” Embedded family offices may be especially difficult to identify by outsiders because they may bear the same name as the parent organization.

Embedded family offices might start to consider investing in venture capital as a means of seeding a corporate innovation effort for closely held corporate entities of which they form a part. In many cases these closely held corporations exist in legacy industries like, transportation and logistics, agriculture, real estate, construction, and manufacturing. As advanced technology becomes more capable of affecting the way operations, supply chains, and value chains in these industries are managed, Embedded Family Offices offer their parent organizations a non-intrusive way of testing the waters with respect to establishing corporate innovation initiatives. The idea here is that the Embedded Family Office can initiate the effort, and if the results are promising after 2 or 3 years, the corporate parent can expand and scale the effort so that it has a more meaningful impact on the corporation’s competitive position and bottomline.

The potential for symbiosis between family offices and emerging managers is obvious: First, many new venture fund managers are pursuing the kind of Systems Investing investment theses that are designed to make a significant, positive difference in the world while taking advantage of and harnessing the unique ability of innovation capital to serve as a catalyst for change in exchange for investment returns. These managers have the knowledge, desire, and social networks to execute their investment strategies successfully and creating great financial returns in the process, but they lack capital to get started; Second, family offices have abundant capital and accumulated knowledge about industries and business relationships that can be additive and complementary to the networks that emerging venture firm managers have cultivated, but lack the knowledge, networks, and personnel to successfully execute an early-stage technology venture capital investing effort.

The bottomline is this: Family offices can accomplish their number 1 objective, preserving and growing multigenerational wealth, by partnering with the right emerging venture capital managers. Moreover, given that venture capital offers the most compelling long-term financial returns AND given the apparent likely future outcomes for private and public markets, according to Austin and Thurston, it seems to me that my proposition that family offices should partner with emerging venture firm managers is a no-brainer.

That leads us to the next question.

How Should Family Offices and Emerging Venture Firms Partner?

I hope I have persuaded family office principals and executives, as well as emerging venture fund managers, that it is in their mutual best interest to find ways to collaborate with one another. Here are nine ways in which a family office could approach investing in the venture capital asset class.

Before delving into tactical suggestions, it is instructive to consider the conclusions reached by Kamal Hassan, Monisha Varadan, and Claudia Zeisberger (HV&Z) in The Pervasive, Head-Scratching, Risk- Exploding Problem With Venture Capital, an article published by Institutional Investor on September 29, 2020. While the article is written with institutional investors – pension funds, funds-of-funds, foundations, and endowments as its target audience, ambitious family offices can take some pointers from the ideas the authors explore.

HV&Z argue that, “The golden rule for investors into the venture asset class must therefore be: Build a portfolio of 500 startups, with 100 companies being the absolute minimum.” They also point out that the average venture fund general partner is highly unlikely to pursue an indexing strategy – the technical jargon for the practice of building a large portfolio with as many holdings as the one HV&Z recommend, it is also pejoratively referred to as “spray and pray” investing in the venture capital community. Be that as it may, they add that, “Diversifying is also hard to execute operationally. Managing a portfolio of 100, let alone 500, investments takes significantly more effort than managing a portfolio of 20 investments. Manpower resource constraints in particular come to mind, as VC funds usually have a surprisingly small number of senior partners and dealmakers.”

HV&Z point out that, “Building a well-diversified portfolio of startups with exposure to at least 500 venture investments is easier than one might expect: Investors who have deployed consistently into venture funds for the past decade without trying to time the market have been able to do so. By investing in three or four funds every year for a decade, you will maintain an ongoing portfolio of around 30 to 40 funds, likely aggregating to more than 500 companies.”

Rather than investing in 30 – 40 funds, HV&Z suggests that this can be achieved by investing in approximately 15 venture firms, and they suggest taking industry and geographic diversification into account to obtain the best results. They point out that this a cherry-picking strategy, and so they urge limited partners to “cover the gaps between their specialized fund strategies with one or more broad-based or index funds, of which a few exist, such as 500 Startups, the AngelList Access Fund, Y Combinator funds, or the Loyal Startup Index Fund.”

I think the rest of the article is worth reading for family office principals and executives sorting through these issues.

The focus of this section of this article is on those 15 – 20 relationships that a family office might seek to establish with emerging venture capital firms. What are the tactical approaches a family office might consider employing to create each of these relationships?

- The Plain-Vanilla LP Commitment Approach: This is the easiest to implement because it simply requires that the family office make a straight-forward decision to invest in the emerging manager’s fund as a limited partner. Depending on how much interest the family office has in learning the inner workings of early-stage technology venture capital investing AND the size of the limited partner commitment, the managers of the venture firm may agree to offer more access than they would normally afford limited partners.

- The Working Capital Loan + LP Commitment Approach: This is a somewhat more involved approach. The easy aspect of this approach is the limited partner commitment that the family office makes. Once more, depending on the goals of the family office, this limited partner commitment may be smaller or larger, with a larger commitment of say 10% of the target fund size for a lead or anchor limited partner role. As I have already stated, while raising their first fund and establishing their venture firm, most general partners lack capital and typically go without a salary for two or more years. An anchor limited partner may commit to invest 10% of the fund target and furnish the general partners with a working capital loan that is secured by the general partners’ future carry from the fund, and payable from the general partners carry on that fund and future funds until such a time that the anchor limited partner has been paid an agreed multiple of the working capital loan. Securing the loan against carry ensures that the general partners do not put at risk the stream of management fees that they’ll need to meet the expenses of running the investment management company that they have set out to build.